Developments in Securities Fraud Class Actions Against U.S. Life Sciences Companies

April 02, 2024

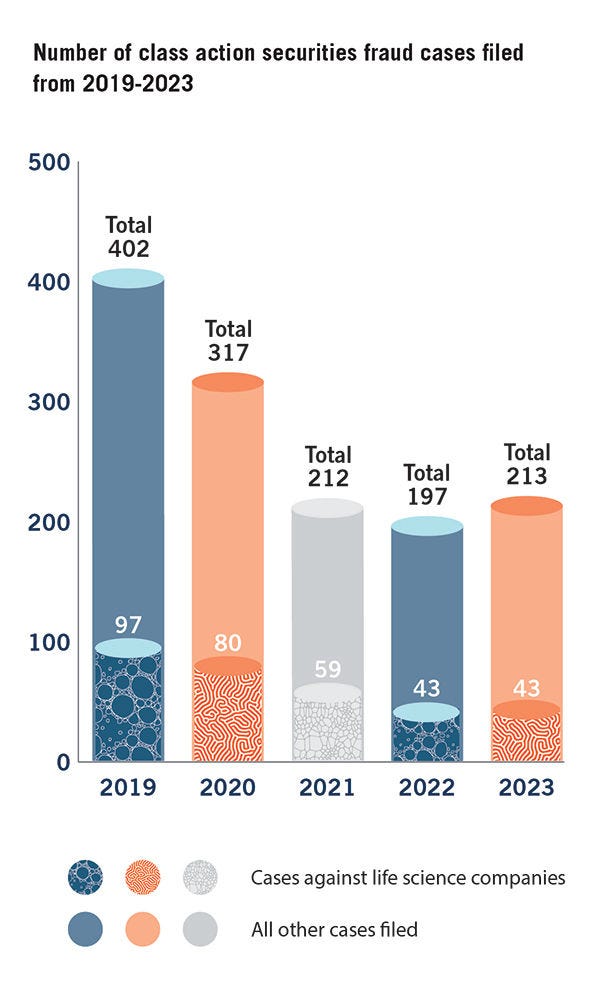

Last year marked an increase in federal securities class action filings, with plaintiffs filing 213 cases in 2023, up from 197 in 2022 and ending an overall decline in filings since 2019. Life sciences companies remained popular targets, accounting for approximately one in five of these filings.1 In this white paper, we examine 2023’s filing and decision trends, providing insights for life sciences companies to prudently navigate the litigation landscape.

Plaintiffs filed a total of 43 securities class action lawsuits against life sciences companies in 2023, which represented almost one in five securities class action lawsuits.

Filings against life sciences companies in 2023 remained stable from the previous year but represent an approximately 50% decrease from five years prior in 2018. Of these cases, the following trends emerged:

- Consistent with historic trends, the majority of suits were filed in the Second, Third and Ninth Circuits, with a 20% increase in suits filed in the Ninth Circuit – 10 in 2022 and 12 in 2023. Notably, the Third Circuit saw a 160% increase in filings from the previous year – from five in 2022 to 13 in 2023. For district courts within these circuits, the District of New Jersey had the most filings, with 10 overall.

- A few plaintiff law firms were associated with almost half of the first filed complaints against life sciences companies: Pomerantz LLP (11 complaints), Glancy Prongay & Murray LLP (9 complaints), Levi & Korsinsky, LLP (7 complaints), and The Law Offices of Frank R. Cruz (6 complaints).

- Significantly more claims were filed in the second half of 2023 than in the first half, with 28 complaints filed in the third and fourth quarters, and 15 complaints filed in the first and second quarters.

An examination of the types of cases filed in 2023 reveals continuing trends regarding the underlying claims from previous years.

- About 46.5% of complaints, or 20 of 43 complaints, involved alleged misrepresentations regarding product efficacy and safety, with many of these cases involving alleged misrepresentations regarding certain negative side effects or the general ineffectiveness associated with leading product candidates, which could potentially impact the likelihood of Food and Drug Administration (“FDA”) approval.

- About 27.9% of the complaints, or 12 of 43 complaints, arose from alleged misrepresentations involving regulatory hurdles, the timing of FDA approval, or the sufficiency of applications submitted to the FDA.

- About 11.6% of the complaints, or five of 43 complaints, involved misrepresentations related to COVID-19 related vaccines, products, or services.

- About 9.3% of the complaints, or four of 43 complaints, alleged misrepresentations regarding purported underlying unlawful conduct that gave rise to a securities fraud claim.

- About 16.3% of the complaints, or seven of 43 complaints, were against non-U.S. issuers incorporated abroad.

- About 34.9% of the complaints, or 15 of 43 complaints, involved alleged misrepresentations related to the company’s financial reporting.

- About 18.6% of the complaints, or eight of 43 complaints, involved alleged misrepresentations of material information made in connection with proposed mergers, sales, initial public offerings (“IPOs”), offerings and other transactions.2

Minimizing Securities Fraud Litigation Risks

Life sciences companies continue to be a popular target for class action securities fraud claims. While many of the companies discussed above were successful in defending against these claims, companies should be cautious and take steps to reduce the risk of being targeted in a securities fraud class action. Below is a list of practices that life sciences companies should consider:

- Companies should strive to avoid any inconsistency in public statements and fight the urge to respond instinctively without identifying known risks or considering non-public information.

- In particular, many life sciences companies encounter regulatory setbacks, such as negative side effects in clinical trials, clinical trial failures, receipt of complete response letters, etc. When these are disclosed to the market, it may trigger a stock price drop. Companies should exercise care when making any disclosures to ensure that they disclose both the positive and negative results, including potentially negative information learned after the preliminary results are issued. Companies should ensure that internal disclosure regimens and processes are well-documented and consistently followed.

- Smaller life sciences companies are susceptible to securities class actions and should work with counsel to ensure that they adopt a disclosure plan. Disclosure plans should not be limited to reviewed and written disclosures made in press releases or SEC filings, but should also include any statements made by executives during analyst calls. Company websites should also be continually updated.

- Life sciences companies are not immune to issues that may cut across all industries, and accordingly they should be prepared to make appropriate disclosures relating to transactions, business prospects, operations, financials, etc. Companies should ensure they are staying informed regarding the acts of third-party contractors and manufacturers, and public statements are consistent with the actions of such parties.

- Courts often have the benefit of hindsight to determine whether a product is defective by considering what defendants could or should have done differently. For example, courts often consider the existence of safer alternatives and the ability of the defendant to eliminate a product’s dangerous characteristics. Companies should consider not only whether a given product is defective on its own, but how it compares to potential alternative designs or formulations and how its benefits balance the risks.

- Because deal litigation and other combinations and partnerships continue with regarding to life sciences companies, material disclosures to investors relating to the transaction should contain detailed explanations about the history of the transaction, alternatives to the transaction, reasons for the recommendation, the terms of the transaction, fairness opinions, and conflicts of interest, among other issues.

- Even if incorporated abroad, life sciences companies that are non-U.S. issuers may be targeted in the U.S. despite events occurring that may not be U.S. specific.

- Regarding statements made in public filings, courts continue to weigh in on opinion statements, and the law is continuing to evolve. Be aware that opinion statements should be reasonably held and not conflict with information that would render the statements misleading.

- Forward-looking information about a drug or device should be clearly identified as such and distinguished from historical fact. Analyst calls and webcasts should also identify certain disclosures as forward-looking statements.

- Risk disclosures that are current, relevant and upfront help to ward off securities class actions. Companies should ensure that public statements and filings contain not only general disclaimers relating to forward-looking statements but also appropriate “cautionary language” or “risk factors” that are specific and meaningful, and cover the gamut of risks throughout the entire drug product life cycle – from development to commercialization.

- Develop and publish an insider trading policy to minimize the risk of inside trades, including 10b5-1 trading plans and trading windows. Class action lawyers aggressively monitor trades by insiders to develop allegations that a company’s executives knew “the truth” and unloaded their shares before it was disclosed to the public and the stock plummeted. Regulators are also cautious that corporate insiders use Rule 10b5-1 plans in ways that are not consistent with the objectives of the rule and will start monitoring 10b5-1 trading plans that are canceled or terminated based on later-obtained material nonpublic information.

Footnotes

1 Throughout this survey, data from prior years is derived from Dechert LLP’s 2023 survey on the same topic. See David Kistenbroker, Joni Jacobsen, Angela Liu, Dechert Survey: Developments in U.S. Securities Fraud Class Actions Against Life Sciences Companies, Dechert LLP (Feb. 2023). The number of securities fraud class actions filed generally and in particular against life sciences companies is based on information reported by Cornerstone Research, Securities Class Action Filings: 2023 Year in Review (last visited Feb. 21, 2024). This survey includes litigation and cases involving drugs, devices, deal litigation, and hospital management. These figures are based on the first complaint filed.

2 It should be noted that the majority of all 2023 filings against life sciences companies fell in more than one category.

View and Download Previous Editions

Related Professionals