Asset Management Spin-Outs — To LLP or Not to LLP: That is the Question

March 12, 2020

Establishing a new fund management business using an LLP is no longer the “no-brainer” default option it once was.

While advantages remain, it's important to evaluate many factors when considering whether to use an LLP or a limited company for the management vehicle.

LLP advantages have eroded

Following its introduction in 2001, the LLP quickly became the vehicle of choice for those looking to start an asset management business. Offering the protection of limited liability, along with the flexibility and tax-planning possibilities of a partnership, the LLP was often a clear choice.

But many of the historic advantages of the LLP have eroded in recent years, leaving many of today’s new managers with a genuine dilemma.

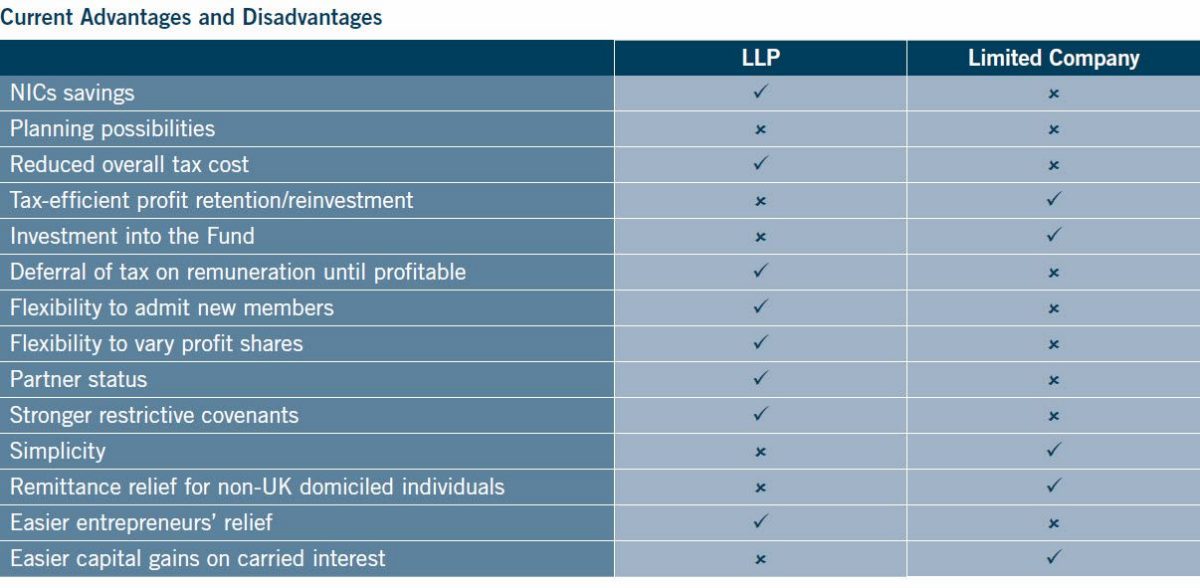

The specific advantages and disadvantages range across various areas.

NICs Savings

Planning Possibilities

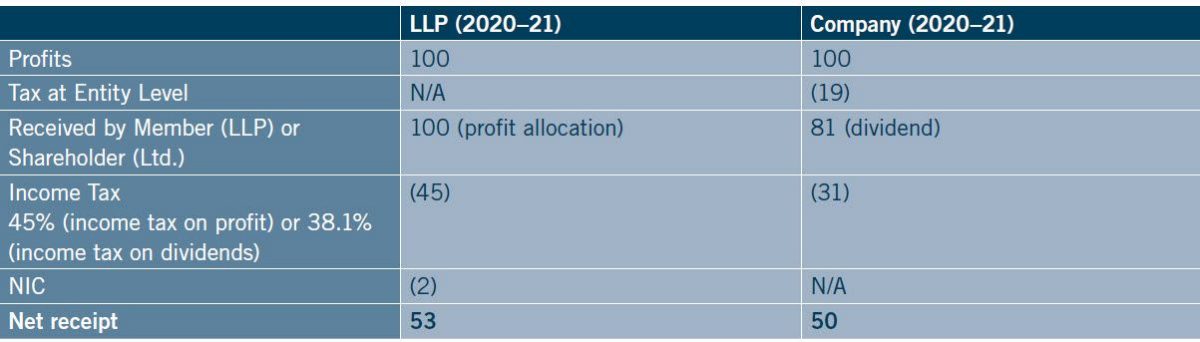

Reduced Overall Tax Cost

An LLP potentially offers a small overall tax saving, though much will depend on personal circumstances.

In the example below, all profits are distributed by a company in the form of dividends (as opposed to salary or bonus, which are taxed at higher rates); and all taxes are paid on dividends/profit share at the highest rates (disregarding any lower marginal rates of tax).

Tax-Efficient Profit Retention/Reinvestment

Deferral of Tax on Remuneration Until Profitable

Flexibility to Admit New Members

Flexibility to Vary Profit Shares

Subject to the terms of the LLP agreement, members of an LLP are free to vary the basis on which the members share in the LLP’s profits. This allows significant flexibility to adjust members’ profit shares on an annual basis to reflect their contributions to the business.

While limited companies have the flexibility to pay discretionary bonuses to reward personal performance, such payments are subject to employer NICs at 13.8 percent (or 14.3 percent if the Apprenticeship Levy is due).

Profits may be distributed to shareholders free of NICs in the form of dividends. However, dividends generally must be paid to shareholders pro-rata to their shareholdings, and varying the proportions in which equity is held is itself ordinarily taxable.

Partner Status

Although seniority or importance to a business established as a limited company is frequently demonstrated through a wide range of impressive job titles, there remains a certain distinction for many to being a “partner” in a business.

Partnership can help create a greater sense of ownership in the business, as well as a club-like atmosphere among the key individuals. Partner status also may serve as an incentive to lateral recruits. The importance of this factor will vary from business to business but is rarely a critical aspect in decision making.

Restrictive Covenants

Simplicity

Although the degree of complexity is principally a result of the commercial arrangements between the principals and with any co-investors, limited companies generally remain simpler, quicker and less expensive to establish than LLPs.

In many cases, particularly where the principals are from non-UK jurisdictions and unfamiliar with LLPs, limited companies are better understood and perceived to be easier to operate.

Remittance Relief for Non-UK Domiciled Individuals

Investing in a limited company may enable business investment relief to be claimed in order to prevent a taxable remittance if:

- The founders are non-UK domiciled individuals claiming the remittance basis. Broadly, it permits such individuals to elect to be taxed in the UK on non-UK source income and gains, only to the extent such income and gains are remitted to the UK

- Such individuals propose to fund the business establishment from non-UK income or gains

An investment in a UK LLP is not a qualifying investment for business investment relief purposes, and would constitute a taxable remittance if funded with non-UK income or gains. Although the potential extension of business investment relief to investments in partnerships has been mooted on a number of occasions since this relief was introduced in 2012, there currently are no plans for such an extension.

Entrepreneurs’ Relief

Carried Interest

Related Professionals

Subscribe to Dechert Updates