DAMITT 2022 Annual Report: Timing and Remedy Risks Grow for Transactions Hit with Significant Investigations

January 23, 2023

Key Facts

United States

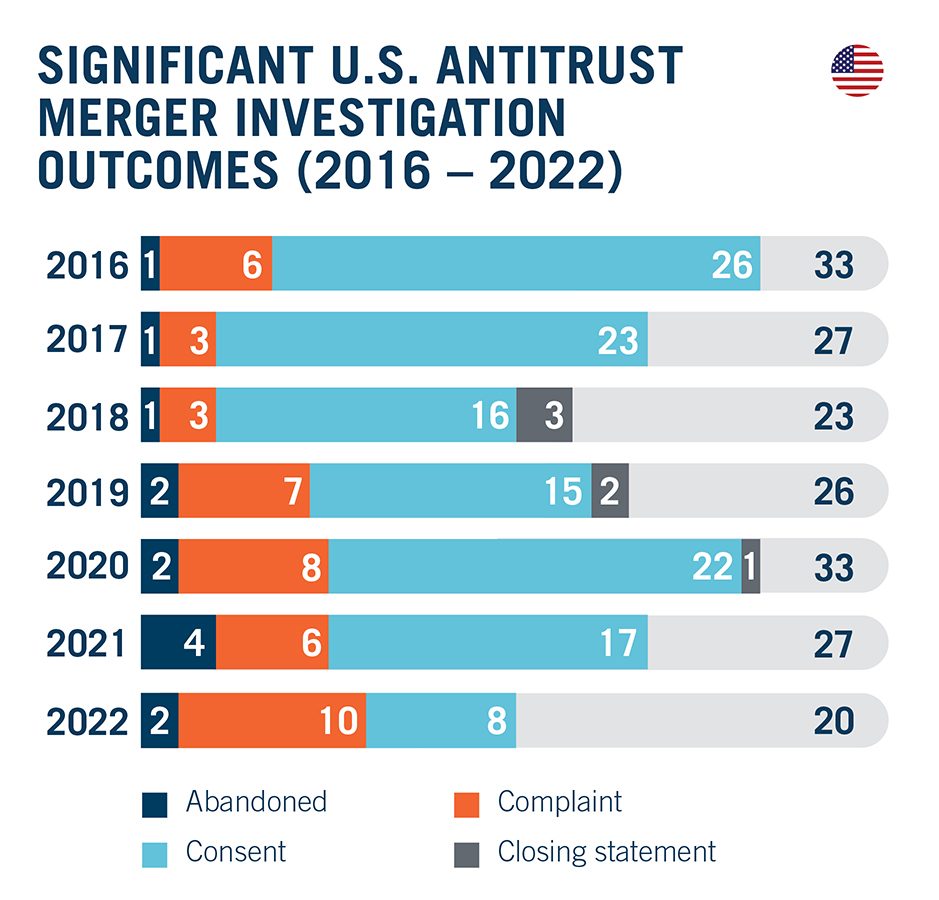

- Sixty percent of significant investigations concluded with a complaint or abandoned transaction in 2022. This shatters last year’s record of 37 percent. The 10 complaints filed in 2022 are also a DAMITT record. Those are strong headwinds for dealmakers heading into 2023.

- Only two significant merger investigations concluded in Q4 2022, making the 20 concluded in 2022 the lowest in DAMITT history. DOJ did not conclude any investigations in Q4.

- The overall intervention rate remains low. Just around 0.5 percent of transactions notified in 2021 had resulted in a concluded investigation as of the end of 2022.

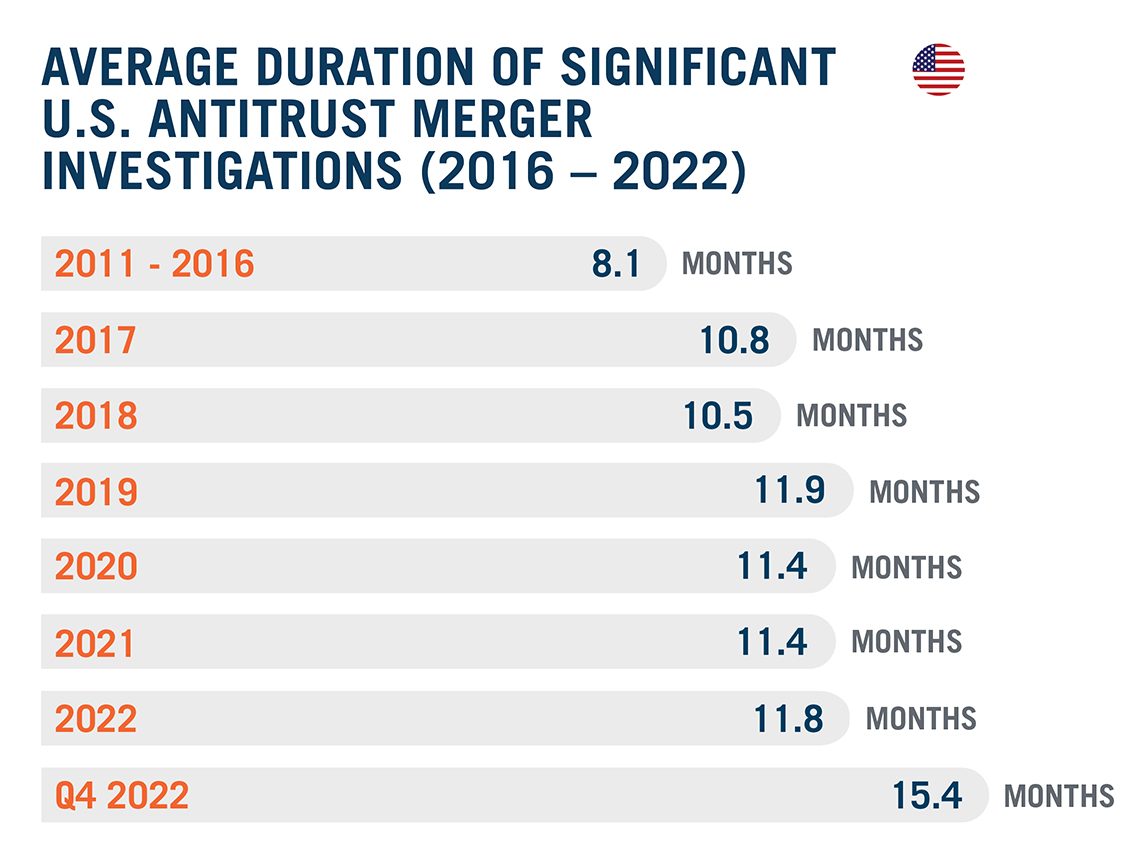

- The average duration of significant investigations ticked up to 11.8 months, just shy of the 11.9-month DAMITT record set in 2019. The Q4 average was 15.4 months but it is based on just two concluded FTC investigations. Still, the risk of a prolonged investigation has grown, especially over the last year.

European Union

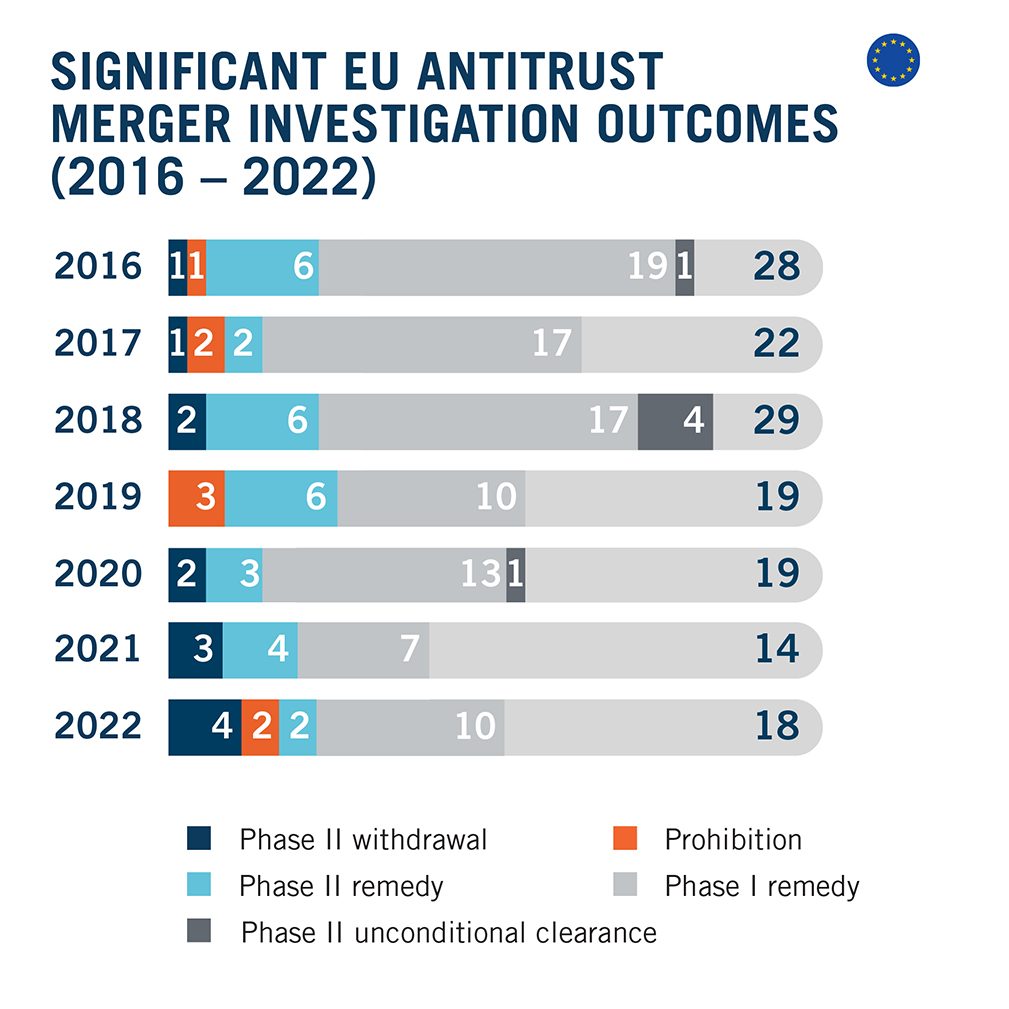

- Thirty-three percent of all significant investigations were blocked by the EC or abandoned by the parties in 2022, with only 25 percent of deals obtaining clearance after a Phase II investigation.

- The number of significant investigations concluded by the EC is slowly picking up, but the number of Phase I remedy cases remains 30 percent below the 2016-2021 average.

- Intervention rates increased in the EU, with 4.9 percent of notified transactions resulting in a significant investigation in 2022. They are not yet back to pre-pandemic levels, though.

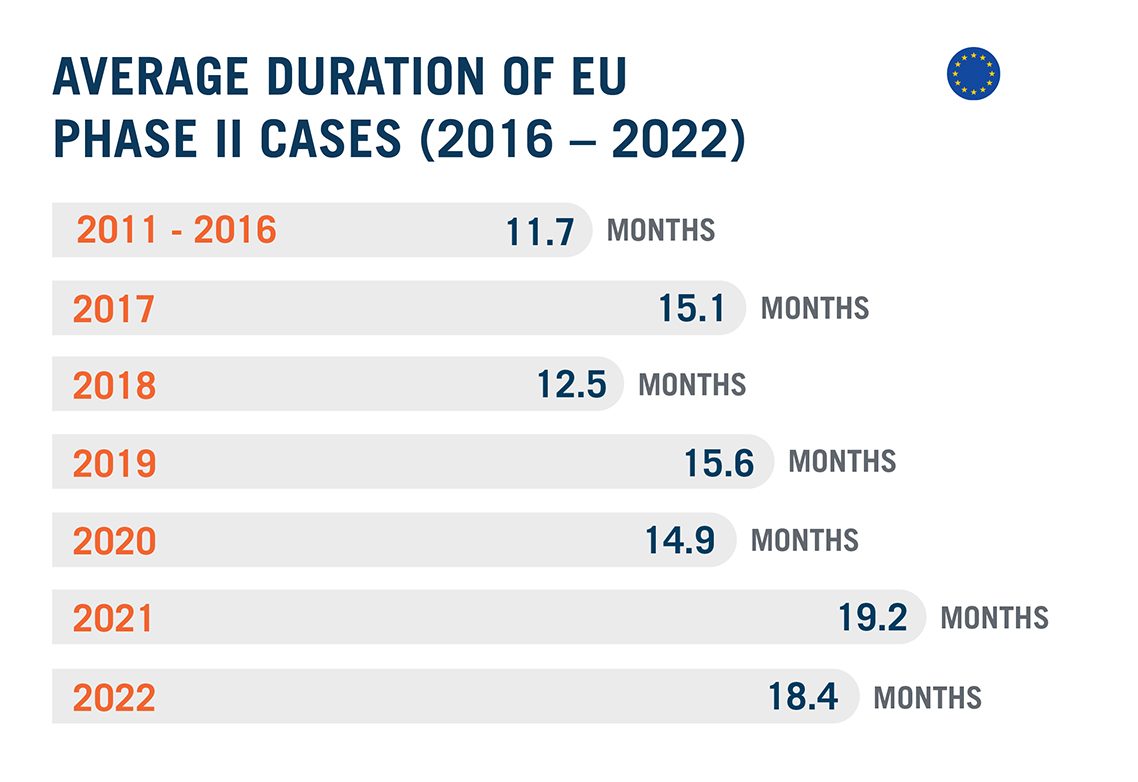

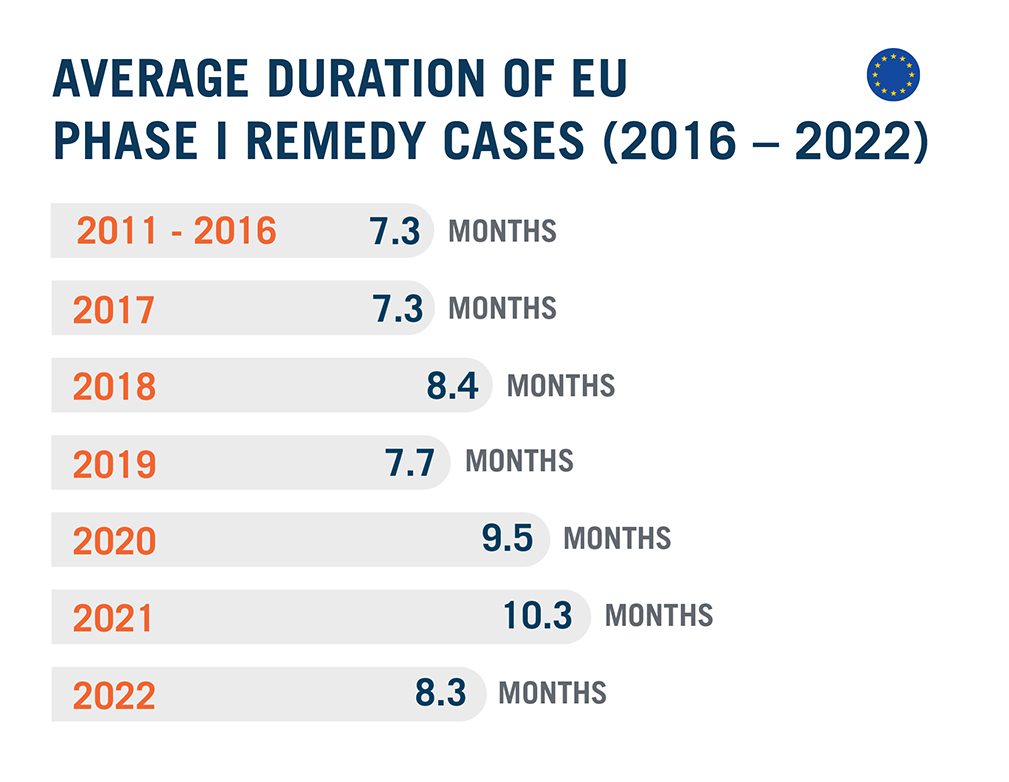

- The average duration of Phase II investigations concluded in 2022 was 18.4 months, nearly one month shorter than in 2021, while average duration of Phase I remedy cases dropped by two months to 8.3 months. New DAMITT data however show that nearly 30 percent of Phase I remedy and Phase II cases have lasted more than 10 and 18 months, respectively.

The U.S. Agencies See Fewer Significant Investigations, But Investigations Pack a Real Punch for Deals Under Scrutiny

We are beginning to sound like a broken record. In our DAMITT 2021 Report, our Q1 2022 Report, and our Q3 2022 Report, we warned that parties to transactions subject to significant merger investigations were more likely to see the FTC or DOJ sue to block their deal or push them to abandon it prior to being sued. Q4 2022 was no exception. Indeed, for all of 2022, a full 60 percent of concluded investigations resulted in either a complaint or an abandoned transaction. That is up from 37 percent in 2021, which was previously a record high. Those are strong antitrust headwinds for dealmakers heading into 2023.

To be clear, there is currently a significant difference between the willingness of the FTC and DOJ to enter consent decrees to resolve merger challenges. In 2022, 40 percent of all concluded significant investigations resulted in a consent decree, with all of those entered by the FTC. By contrast, the DOJ has not entered into a single settlement to resolve a significant investigation since DOJ Assistant Attorney General Jonathan Kanter began warning, shortly after taking office in November 2021, that investigations resolved with merger remedies should be the “exception, not the rule.” DOJ also did not report any concluded investigations in the last quarter. It is possible, of course, that DOJ has concluded significant investigations that have flown under the radar without a complaint or settlement, but the absence of any reported investigations is still notable.

Only two significant investigations concluded in Q4 2022, which itself is a DAMITT record low for the fourth quarter. The last quarter of the year often sees more activity, so the relatively low number of concluded investigations in Q4 2022—matched with the low number in Q3 2022—is a development worth following. It is unclear whether this represents a drop in overall activity or reflects the increased difficulty of getting significant investigations closed.

As part of FTC and DOJ efforts to block more mergers, 2022 ended with ten litigation complaints filed to block transactions, the most observed in a single year since DAMITT started tracking in 2011. Combined with the low number of concluded investigations, this figure paints a stark contrast for deals that do see significant investigation activity.

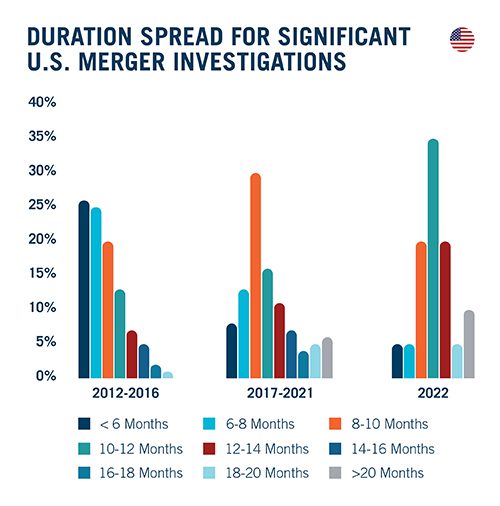

Timing remains a considerable risk for transactions that see significant merger investigation activity as well. The average duration of a significant investigation ticked up to 11.8 months in 2022, just shy of the DAMITT record of 11.9 months set in 2019. The average duration for Q4 2022 was a jaw-dropping 15.4 months, but this figure warrants some caution. Only two matters concluded in Q4 2022, and one of those—Tractor Supply Co. / Orscheln Farm & Home LLC—lasted 20 months. While this outlier skewed the quarter average, it is worth asking: are there more “outliers” these days? Based on the data, the answer is a resounding yes.

Between 2012 and 2016, for example, DAMITT data do not show a single significant merger investigation with a duration above 20 months. This changed between 2017 and 2021, when six percent of concluded investigations lasted more than 20 months. This shift appears to coincide with increased skepticism of behavioral remedies under the Trump administration. The trend has continued into the current administration. In 2022, ten percent of investigations took 20 months or more.

The U.S. agencies still see far fewer durations above 20 months than the EU, but the data show an unmistakable shift towards longer durations. This shift also is evident in the waning numbers of durations below 8 months. In this case, the rising tide has appeared to lift all durations, which is evident in a 2022 median duration of 11.3 months—the highest median in DAMITT history.

Here, it is important to keep in mind that the average duration of a significant investigation only measures the time from the initial merger filing to a settlement, abandoned transaction, closing statement, or complaint. Parties also may need to plan for time to litigate to defend the transaction for investigations that could conclude with a complaint. Litigation in federal court has lasted an average of just under 10 months between the complaint and decision over the last two years. The average was pushed up from nine months by Penguin Random House / Simon & Schuster, which took 12 months to litigate from complaint to decision.

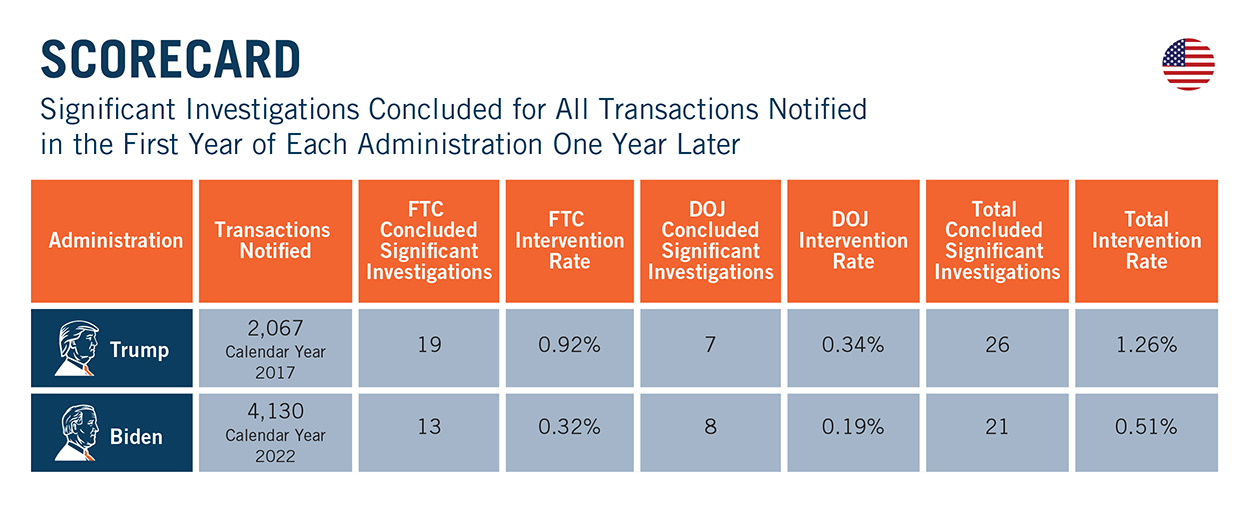

As a silver lining, U.S. intervention rates remain relatively low. Of all deals notified in 2021, only 0.5 percent resulted in a concluded significant investigation. This is less than half of the intervention rate under the Trump administration at the same point in time.

At the same time, a leading driver of this low intervention rate was the 4,130 transactions notified in 2021, which was more than double the 1,965 recorded in 2020. In 2022, by contrast, there were 2,496 notified transactions, which was closer to historical norms. Combined with increased agency budgets for enforcement, we expect an increase in the intervention rate looking forward.

Deals Subject to a Significant Investigation in the EU Face Higher Risks of Negative Outcomes and Longer Durations

In the EU, like the U.S., deals under investigation are facing significant headwinds, with 33 percent of significant investigations being blocked by the EU Commission (“EC”) or abandoned by the parties in 2022. Six deals were abandoned or blocked following a Phase II investigation, the highest number ever recorded since DAMITT started tracking in 2011 and nearly 200 percent above the average between 2011 and 2021. Although deals may in theory be abandoned for various reasons, regulatory challenges were explicitly mentioned as the reason for the termination of the Nvidia / Arm transaction, and the Kronospan / Pfleiderer Polska and Kingspan Group / Trimo transactions were reportedly abandoned due to EC concerns and looming prohibitions.

If 2022 trends were to continue, a deal sent to Phase II would have only a 25 percent chance of being cleared by the EC, down from 65 percent between 2016 and 2021.

Looking at the number of significant investigations more broadly, the EC is slowly picking up pace and concluded 18 significant merger investigations in 2022. While it is an increase compared to the near-record low of 2021, this is still 13 percent below the average number of significant investigations concluded yearly between 2016 and 2021. Of note, the drop is entirely driven by a sharp decrease in Phase I remedies cases, while the number of Phase II cases remains in line with previous years.

As a positive note, compared to the number of filings, the proportion of deals undergoing a significant investigation remains relatively low, at only 4.9 percent. While this is up 1.4 point from 2021, it is still below the 5.7 percent average for the period between 2016 and 2021.

In that respect, it should be noted that although one of the mergers prohibited in 2022, Illumina / Grail, was referred to the EC based on the new interpretation of Article 22 of the EU Merger Regulation, which now allows Member States to refer deals to the EC that fail to meet EU and national reportability thresholds, this policy change has not brought about the flood of new significant investigations that observers feared. So far, Illumina / Grail is the only case in which that provision was used. However, as the General Court of the European Union confirmed the validity of the new interpretation of Article 22 in a judgment dated 13 July 2022 (case T-227/21), it is still possible that the number of such cases will pick up in the future, especially in the sectors targeted by the EC guidance (tech/digital and pharma).

In terms of timing, the diverging trends identified in DAMITT Q3 2022 Report between Phase I remedy and Phase II cases continues. The duration of Phase II significant investigations reached 18.4 months in 2022, slightly below the average duration recorded in 2021 but still nearly 20 percent above the average between 2016 and 2021.

Conversely, duration of Phase I remedy cases dropped to 8.3 months, four percent below the average between 2016 and 2021.

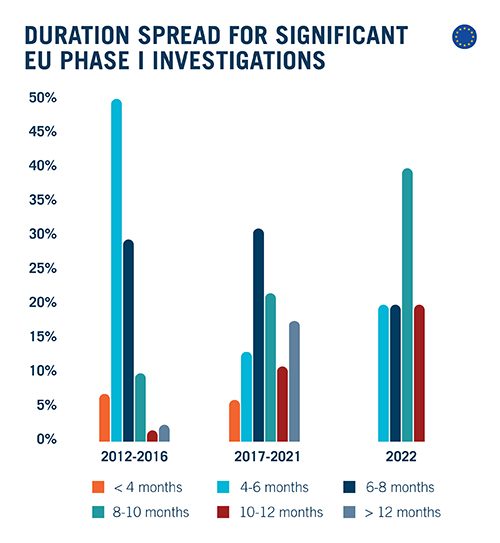

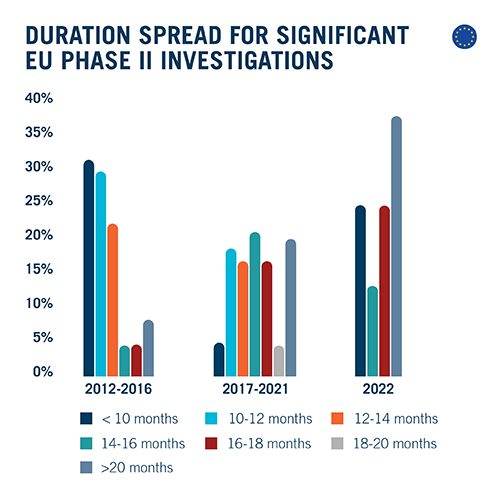

Because averages alone can be deceptive, it is also worth taking a closer look at the spread of durations between transactions over time. This analysis highlights a general shift toward longer investigations over time, both for Phase I remedy and Phase II cases.

For Phase I remedy cases, 49 percent of investigations lasted between four and six months for the period between 2012 and 2016.

By contrast, the majority of Phase I reviews lasted more than eight months between 2017 and 2021. The same trend continued into 2022. On the higher end, while only three percent of cases lasted more than 12 months between 2012 and 2016, nearly 20 percent have reached at least 12 months between 2017 and 2021, even as no case lasted that long in 2022.

Turning to Phase II, 83 percent of Phase II investigations concluded in less than 14 months between 2012 and 2016, with 31 percent lasting less than 10 months. Between 2017 and 2021, however, only 40 percent of cases lasted less than 14 months, dropping to 25 percent in 2022. On the higher end, while only eight percent of cases lasted more than 18 months between 2012 and 2016, this proportion reached 24 percent between 2017 and 2021 and 38 percent in 2022. Considering the limited number of Phase II cases concluded each year by the EC, looking at these longer time periods helps provide a more accurate picture of duration trends.

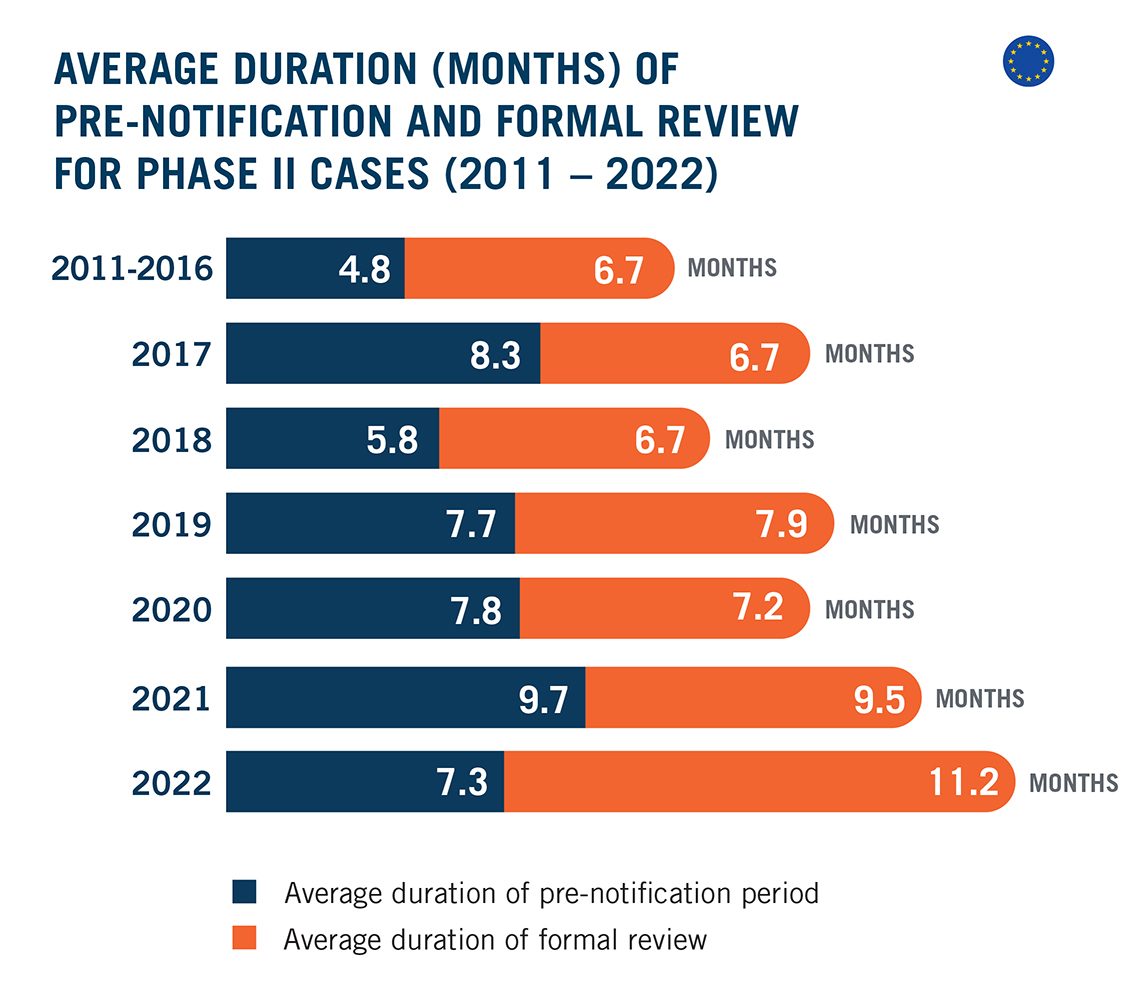

For the EU, it important to note that the pre-filing period during which parties typically engage in discussions with the EC usually accounts for approximately half of the total duration of a Phase II case. This remains true in 2022. And the lower average recorded by DAMITT is mainly due to one case, which was announced and notified on the same day. Excluding this transaction, the average duration of pre-notification reaches a closer to average 8.3 months.

Significant investigations concluded in 2022 however show a significant increase in the duration of the formal review period – even though it is normally capped by the EU Merger Regulation, reaching a record high of 11.2 months. This longer duration is due to the EC’s increased use of its statutory powers under the EU Merger Regulation, which allow case teams to agree to “voluntary” extensions with the merging parties and issue “stop the clock” orders. The EC granted voluntary extensions in all but one Phase II investigation concluded in 2022. Eighty-eight percent of significant investigations resolved in 2022 were suspended, for an average of nearly six months. This average is, however, driven up by three deals that were announced during the pandemic, so time will tell whether this is a new feature of EU merger control or just a temporary adverse effect of Covid-19.

Conclusion

Parties to transactions subject to significant merger investigations continue to face an elevated risk of seeing their deal blocked or abandoned on both sides of the Atlantic, even if the intervention rate shows relatively few deals may receive close scrutiny. To ensure the ability to defend their deals through a potential investigation, parties to the average “significant” deal in the U.S. should plan on at least 12 months for the agencies to investigate their transaction and may want to add on additional time to address the continuing uncertainty at the agencies. Parties should also plan for another nine to 10 months if they want to preserve their right to litigate an adverse agency decision. On the EU side, parties to transactions likely to proceed to Phase II investigations should allow for at least 20 months from announcement to clearance and should not rely on the theoretical deadlines provided for in the EU Merger Regulation, even after a deal has been formally notified. If the investigation is likely to be resolved in Phase I with remedies, parties should plan on around nine months from announcement to a decision.

Related Professionals

Subscribe to Dechert Updates