DAMITT 2020 Report: Merger control in Germany and France

February 04, 2021

For the first time, our antitrust/competition practice has expanded the Dechert Antitrust Merger Investigation Timing Tracker (DAMITT) to include Germany and France. The new segment, supplements DAMITT’s U.S. and EU coverage with comprehensive analysis of key merger control indicators before the German Federal Cartel Office (FCO) and the French Competition Authorities (FCA), including the duration of merger control reviews in both jurisdictions and the outcome of the competition authorities’ review.

Commenting on the report, the Head of the Mergers Unit at the FCA welcomed “this unique initiative from Dechert”.

Both the French and German authorities are particularly active in merger control at the member state level within the EU. Companies should keep these jurisdictions on their radar in planning their next transaction, using DAMITT data as a guidepost.

Fast Facts

Germany

- The number of filings declined sharply in the spring but recovered later in the year.

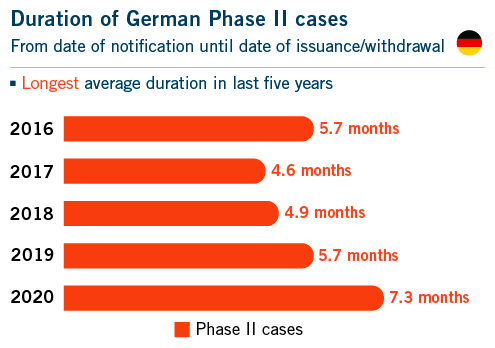

- The average duration of merger investigations that proceeded to Phase II was the longest in the last five years, increasing from 5.7 months in 2019 to 7.3 months in 2020.

- The long-awaited reform of the German Act against Restraints of Competition, which entered into force in January 2021, has brought about significant changes to the German merger control regime. The number of transactions that need to be notified in Germany is expected to decrease by at least one third due to this reform.

- The expected decrease of notifications will free up resources at the FCO, allowing the authority to focus on transactions that pose substantive risks. In line with that aim, the statutory review period in Phase II cases has been extended from four to five months.

France

- The number of merger control decisions issued by the FCA sharply decreased, down by 28 percent in 2020 compared to 2019. This decrease was likely due in part to the impact of the COVID pandemic on the number of notifications.

- There was no relaxation in merger control standards, though: the number of significant investigations (Phase I with remedies and Phase II) increased by 22 percent compared to 2019 and the FCA issued its first prohibition decision ever.

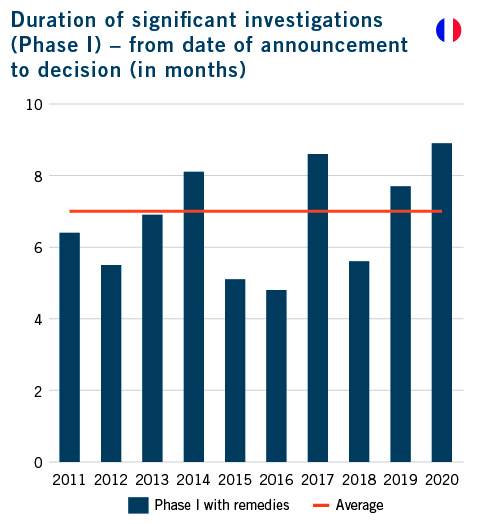

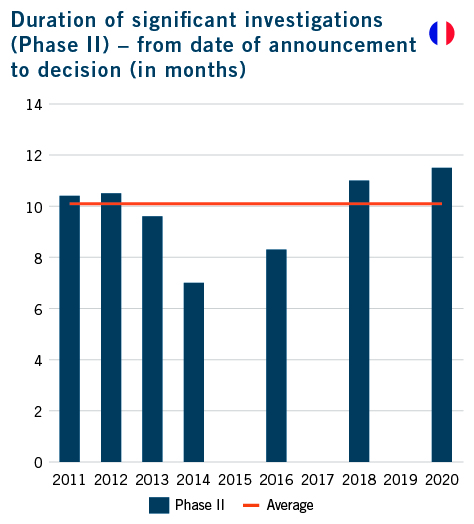

- The duration of investigations increased to an average of 8.9 months for Phase I with remedies and 11.5 months for Phase II, due in part to an increase in the duration of pre-notification talks.

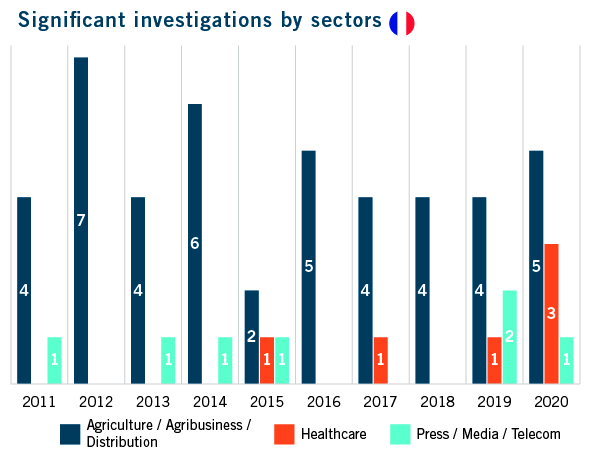

- Consistent with prior years, and further augmented by the pandemic, the retail sector retained the top spot for FCA significant investigations. However, significant investigations among the healthcare, telecoms and media sectors are increasing, reshaping trends in FCA review.

An Uneven Year Followed by a Major Reform

Looking Back

In 2020 the total number of notifications to the FCO declined by around 14 percent (from about 1,400 in 2019 to about 1,200 in 2020) on an annual basis.

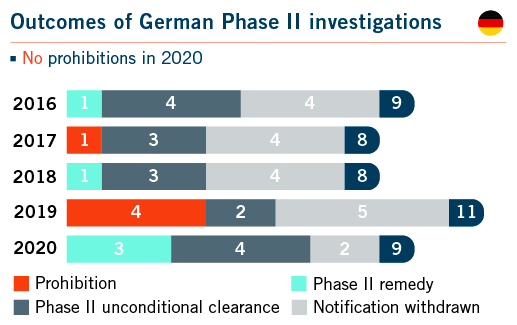

While notifications declined in 2020 compared to 2019, there was a strong recovery in the second half of the year which eventually ran out of steam in December. The FCO concluded nine Phase II cases in 2020, two less than in the previous year. Four of those cases were unconditionally cleared, three were cleared with remedies, and in two cases the deals were abandoned.

There were no outright prohibitions. However, companies often abandon deals in advance of an official decision if the FCO indicates to them that it is preparing to block their transaction.

As in previous years, last year’s Phase II cases related to a large number of diverse industry sectors: the FCO opened in-depth investigations in respect of deals in the cinema, food retail, locomotive, hospital, furniture, car workshops and agricultural products industries.

In 2020 the average duration of merger investigations that proceeded to Phase II increased to 7.3 months (from 5.7 months in 2019). This was the longest average duration recorded in the last five years. Although many expected reviews of complex transactions to take longer in 2020 due to the challenges involved in transitioning to remote work during the pandemic, it is worth noting that less than one percent of transactions notified in Germany are subject to an in-depth Phase II investigation. As such, variations in year-over-year averages are typically the result of specific individual circumstances of the cases reviewed by the FCO. Moreover, a COVID-related temporary extension of the FCO’s merger review deadlines expired in the summer without having had any noticeable effect.

Looking Ahead

A significant reform of the German Act against Restraints of Competition entered into force on January 19, 2021. The reform concerns multiple areas of antitrust enforcement and includes important changes to the German merger control regime. These changes are expected to have a substantial impact on merger control statistics in years to come.

Under German merger rules, transactions require merger control clearance if certain turnover thresholds are exceeded. The new law includes substantial increases to the domestic turnover thresholds.

A notification will now be required if:

- The parties’ combined worldwide revenues exceed €500 million (unchanged);

- one party to the transaction achieves turnover of more than €50 million in Germany (previously €25 million); and

- another party to the transaction achieves revenues of more than €17.5 million in Germany (previously €5 million).

These increases are expected to reduce the number of reportable transactions by at least one third. This will significantly ease the regulatory burden on investors acquiring small German companies or international companies who generate minor turnover in Germany. In addition, the reform is expected to free up resources at the FCO, thus allowing the authority to focus on transactions that pose substantive risks. In line with that aim, the statutory review period in Phase II cases has been extended from four to five months.

Another amendment that will shape German merger control enforcement going forward relates to successive acquisition strategies. The amendment introduces a new provision that allows the FCO to capture successive acquisitions of smaller companies even if the jurisdictional thresholds are not met. The rationale is to enable the FCO to monitor developments in specific economic sectors if it has objective reasons to believe that additional consolidation may harm competition. The FCO can order a company to notify all acquisitions in certain sectors (following a previous FCO sector inquiry), provided that the acquirer’s worldwide revenues exceed €500 million and its domestic market share exceeds 15 percent. The duty to notify only applies to transactions where the target company’s worldwide revenues exceed €2 million and if at least 66 percent of the target’s worldwide revenues are achieved in Germany.

COVID impact on French merger review

2020 has been an anomalous year for merger control in France. Although the pandemic impacted the French merger review process in terms of the number of reportable deals and the duration of investigations, it did not prevent the FCA from issuing its first prohibition decision ever.

The report is based on a comprehensive analysis of all “significant merger investigations” in France, defined as reportable mergers under the French merger control regime which either (i) were cleared in Phase I with commitments under Article L. 430-5 III of the French Commercial Code (FCC), or (ii) went through a Phase II investigation under Article L. 430-6 of the FCC, irrespective of the outcome of the review. These significant investigations correspond to deals which were deemed to raise competition issues by the FCA and therefore subjected to increased scrutiny.

DAMITT also analyzes the duration of merger control reviews in France (from the date of the announcement of the transaction1 to the FCA’s final decision) and the outcome of the review.

Significant drop in the number of decisions, without any impact on the standard of review

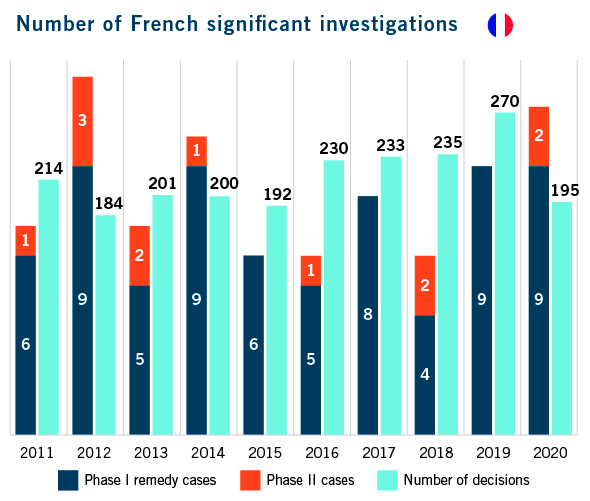

After reaching a peak in 2019, the number of mergers assessed by the FCA in 2020 was at its lowest levels of the past 10 years. Only 195 decisions were issued in 2020, compared to 270 in 2019.

The reason for this sharp 28 percent decrease is likely to be found in the pandemic crisis, which resulted in a decrease in the number of reportable deals. While only 15 deals were notified to the FCA in June (just after the first lockdown period in France), compared to an average of 23 notifications per month in 2019, the figures were back closer to normal by the end of the year, with 23 deals notified to the FCA in November. December totals are not yet available but are expected to be similar.

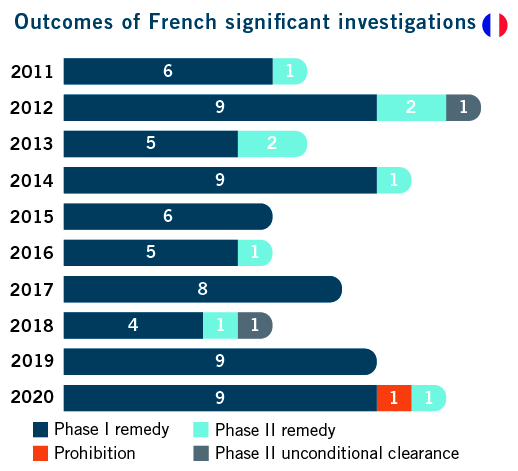

The pandemic did not result in any relaxation in merger control standards, though. The number of significant merger investigations showed a 22 percent increase relative to 2019, with nine Phase I remedy cases and two Phase II cases.

In addition, two of the transactions filed in 2020 (on 10 April 2020 and 14 September 2020 respectively) are still currently undergoing a Phase II investigation.

The high standards of the FCA are also reflected in the outcome of the significant investigations. In 2020, the FCA issued its first prohibition decision ever, blocking an acquisition by a large French supermarket chain in the retail sector (Decision No. 20-DCC-116). Remedies were also imposed in the other Phase II case that was decided by the FCA during the year.

Duration of the French significant investigations reaches new heights

Under French merger control rules, the FCA’s Phase I must be completed within five weeks (25 working days) from the filing. In case commitments are submitted, or if the parties request to suspend the procedure, the review can be extended by two additional weeks. This theoretical deadline does not, however, take into account pre-notification talks, which – although theoretically not mandatory – are de facto required by the FCA. The possibility for the FCA to “stop the clock” if the notifying parties fail to provide requested information before the deadline can also increase the actual duration of Phase I investigations.

Against this background, on average, Phase I exceeded six months over the past ten years when taking pre-notification talks into account. 2020 established a new record in that regard. Phase I remedy cases were cleared in 8.9 months on average, from the date of the deal announcement to the final FCA decision, up 16 percent compared to 2019 (7.7 months). This increase results both from longer pre-notification talks (adding two weeks to the timing on average) and an increase of almost three weeks for the Phase I investigation itself. While other factors may also have played a part, the pandemic likely explains part of the additional delays.

If at the end of Phase I, the FCA considers that the deal may cause serious harm to competition, it can initiate an in-depth investigation (Phase II), which must be completed within 13 additional weeks (65 working days), plus up to 20 working days if commitments are offered. Another 20-day period can be added if the FCA or the parties request a suspension of the procedure, with the overall limit of 21 weeks (105 working days) in total for Phase II. However, this theoretical deadline again excludes de facto mandatory pre-notification talks and the possibility for the FCA to stop the clock when it considers that necessary information has not been provided by the notifying parties.

Although the limited number of Phase II investigations each year makes it difficult to draw definitive conclusions, the duration of the two Phase II cases completed by the FCA in 2020 does show a significant increase compared to 2018 (no Phase II cases in 2019). Phase II investigations averaged 11.5 months from announcement to decision, up 5 percent compared with the 11-month average of 2018.

Again, the pandemic may be to blame for part of this increased duration, although in this case it is also driven by the record-high 13.8-month investigation that resulted in the first prohibition decision issued by the FCA. In comparison, and despite the imposition of remedies, the other Phase II investigation conducted by the FCA lasted only eight months, i.e., less than the average duration for a Phase I case with remedies.

Merger review: area of the FCA’s activity mainly focused on the retail sector

Due to the specific (and much lower) thresholds applicable to the retail sector, deals in this area represent a significant proportion of all mergers examined by the FCA, accounting for between 39.5 percent in 2015 and 66 percent in 2019. 2020 does not depart from this trend, as the COVID pandemic led the FCA to examine a large number of transactions involving retail brands facing economic difficulties (see FCA, press release dated 23 December 2020).

This predominance mainly increases the number of simplified procedures (i.e., unproblematic, expedited investigations) before the FCA, where retail accounts for 78 percent of all decisions over the past ten years. But it is also reflected in significant investigations, as the FCA pays heightened attention to mergers that can result in a price increase for essential goods and staple foods to the detriment of consumers. Cases involving retail and agriculture/agribusiness thus represented often more than 50 percent of significant investigations each year for the past decade.

However, recent years have seen an increased focus on the health sector, which accounted for six significant investigations since 2015, and three in 2020 alone. Press, media and telecommunications have also been a focus for the FCA. In these cases, the FCA’s review in the context of merger control rules mirrors its priorities in terms of antitrust enforcement.

Enforcement in the digital sector has been limited, with only one Phase II case in 2018 (relating to the merger of the two online platforms SeLoger.com and Logic-Immo.com, both specialized in property advertising). This may be due to the large number of digital deals that fall below the (relatively high) French merger control thresholds. As a consequence, the FCA has expressed its extreme willingness to refer mergers to the European Commission under its new interpretation of Article 22 of Regulation No. 139/2004, which would enable national competition authorities to take “into account the acquisition practices of certain players and operations that currently fall ‘below the thresholds’ despite affecting competitive market dynamics are subject to tighter control” (see FCA, press releases dated 23 December 2020 and 9 January 2021). This new tool could have an impact on merger control in France going forward.

Footnotes

1) Please note that date of the formalization of the transaction, as retained in the FCA decision (e.g. signing, firm offer letter), was used as a proxy for the announcement date.

Related Professionals