DAMITT Q2 2022: Is Merger Enforcement Taking a Conservative Turn?

July 26, 2022

Key Facts

United States

- The agencies sued to block fewer transactions, both relatively and in absolute terms. After only 17 percent of concluded significant investigations settled last quarter, two-thirds settled in Q2 2022. All FTC significant investigations were concluded with unanimous consensus votes.

- The average duration of significant investigations concluded in Q2 2022 dropped two months to 10.7 months. The last time the annual average duration dropped below 11 months was 2018.

- By the end of Q2 2022, the FTC and DOJ had only concluded 18 significant investigations into the nearly 5,500 HSR filings made between January 2021 and June 2022.

- The percentage of HSR filings resulting in concluded significant investigations continues to fall and is hovering below one percent.

European Union

- After increased activity in Q1, the EC slowed down and concluded only three significant investigations in Q2 2022. Only nine significant investigations have concluded so far in 2022, a near-record low.

- Compared to 2020 and 2021, there has been a marked decrease in the proportion of filed deals resulting in a significant investigation. Only three percent of deals notified in 2021 resulted in a significant investigation, compared to six percent for deals filed in 2020.

- The duration of significant investigations continues to trend high, averaging at 9.4 months for Phase I with remedy cases and 19 months for Phase II cases over the last six months.

Fewer Significant U.S. Investigations Result in Challenges and the Average Investigation Duration Falls

In both our DAMITT 2021 Report and our Q1 2022 Report, we warned that parties to transactions subject to significant merger investigations were more likely to see the FTC or DOJ sue to block their deal or push them to abandon it prior to being sued. What a difference three months make.

The data still show an elevated risk that a significant merger investigation will result in a lawsuit to block the deal or an abandoned transaction. For the first half of 2022, just over 50 percent of significant investigations resulted in an agency lawsuit or an abandoned deal. While still historically high, this is substantially lower than the 83 percent of significant investigations that met the same fate in Q1 alone. The proportion of complaints and abandoned deals is trending down, at least over the last quarter.

Unlike Q1 2022, when only one of six significant merger investigations was resolved through a settlement, a full two-thirds of the nine investigations concluded in Q2 2022 ended in a consent decree. Notably, each of those settlements were concluded by the FTC and not the DOJ. As a result, it is not clear that there has been any change of view at the DOJ, where DOJ Assistant Attorney General Jonathan Kanter has previously stated that investigations resolved with merger remedies should be the “exception, not the rule.” Yet the DOJ was generally quiet in Q2 2022, concluding only one significant investigation as compared with eight from the FTC. The absence of DOJ settlements has been largely accompanied so far by silence rather than a flurry of complaints.

The average duration of significant investigations dropped nearly two months in Q2 2022 to 10.7 months. Of note, the median also was 10.7 months, indicating that the average is not being influenced by any extreme outliers. When combined with the higher average duration of investigations in Q1, the average duration for the first half of 2022 was 11.5 months, or just slightly above the average from the prior two years.

The average duration of a significant investigation that concluded with a complaint in the first half of 2022 was 11.9 months, while the average duration of a significant investigation that concluded in a consent was 10 months. This data unexpectedly indicates that the FTC may be speeding up significant investigations resulting in a consent agreement.

The longer average duration of matters that result in a complaint is notable given April 2022 statements from the DOJ Principal Deputy Assistant Attorney General that DOJ may seek “faster access to courts” in some cases, because “[t]here are some problems you can see from outer space” and DOJ does not have “to wait one or two years” for parties to comply with a second request before filing a complaint. Along those lines, the only merger challenge filed by DOJ in Q2 2022 concerned Booz Allen Hamilton’s proposed acquisition of Everwatch, which was only publicly announced 3.5 months earlier.

There are reasons, however, not to draw too many inferences from Booz Allen Hamilton/Everwatch, which was the only significant investigation concluded by DOJ in Q2 2022. Most notably, the complaint in that matter alleges a time-sensitive violation of the Section 1 of the Sherman Act, which is not common in merger challenges. In addition, public filings indicate that this deal was notified several months before it was publicly announced, likely based on a letter of intent. As a result, we would caution against inferring that DOJ is proceeding more quickly in most cases based on this distinct outlier. Indeed, this transaction is the only transaction notified between June 2021 and June 2022 that has been the subject of a significant investigation concluded by DOJ as of the end of Q2 2022.

To the extent there is a pattern here, the data suggest that DOJ is increasingly willing to bypass steps in the formal HSR process where it perceives parties may be playing procedural games with the timeline. In Booz Allen Hamilton/Everwatch, for example, the buyer pulled-and-refiled its HSR filing a highly unusual four times before DOJ issued second requests. DOJ then filed its complaint alleging short-term harms to a competitive-bid process before the parties substantially complied with their second requests. Similarly, in Cargotec/Konecranes, DOJ only informed the parties it would file a complaint to block the transaction after the parties delayed complying with their second requests for more than 18 months after their deal was announced. For that deal, the DOJ Principal Deputy Assistant Attorney General said: “[W]hat we saw with our staff was that the protracted posture of the merger review was already having an effect on incentives to compete that was creating uncertainty in the market." The same logic presumably applied to DOJ’s view of the four pull-and-refiles in Booz Allen Hamilton/Everwatch. In other words, where DOJ perceives that parties are using stall tactics to slow down its review, it may be more likely to proceed to court with a complaint.

The nine significant investigations concluded in Q2 2022 are slightly above the average observed for second quarters over the four prior years but seem low given the tidal wave of HSR filings observed for well over a year now. The number of significant investigations concluded in the first half of 2022, for example, is below the number concluded in the first half of 2020, despite many fewer filings. This small number of concluded investigations could be a sign that the agencies have limited resources for conducting additional significant investigations without larger budgets, but it also could be an indication that more transactions have become ensnared in prolonged investigations that have yet to conclude.

EC Concluded Few Significant Investigations, Average Duration Remains Stable

After increased enforcement activity in Q1 2022, we saw a marked decrease in Q2 2022 with only three significant investigations concluded this quarter. While slightly higher than the number of significant investigations concluded in H1 2021, this is more than 20 percent below the average number of significant investigations concluded in the first half of a year since 2016.

Only one transaction, Kingspan Group/Trimo, underwent a Phase II investigation until the deal was ultimately abandoned in Q2 2022. This is significantly lower than the five Phase II cases concluded in Q1 2022. Three transactions are however currently subject to an in-depth investigation. As such 2022 could still conclude with an above average number of Phase II decisions.

The new abandoned deal in Q2 2022 takes the proportion of significant investigations concluded in the first half of 2022 and resulting in a prohibited or an abandoned deal to 44 percent. While this is lower than the 50 percent of significant investigations that met the same fate in Q1 alone, it still indicates a heightened risk for deals taken to Phase II. This statistic should, however, not be overinterpreted as, at the same time, the number of deals triggering a significant investigation is trending downward (see next section on intervention rates).

Turning to duration, the only Phase II investigation concluded in Q2 2022 took 20.3 months, bringing the average length of Phase II cases concluded in H1 to 19 months, broadly in line with the 2021 average. Excluding the Hyundai Heavy Industries Holdings/Daewoo Shipbuilding & Marine Engineering transaction, which was ultimately abandoned in Q1 2022 almost 36 months after announcement, the average stabilizes at 15.6 months, which is more in line with 2019-2020 average durations.

The duration of the Kingspan Group/Trimo review also supports the trend highlighted in our Q1 2022 Report, showing that Phase II investigations lasting more than 20 months from announcement have a higher risk of being ultimately blocked or abandoned.

The EC concluded two cases with remedies following a Phase I investigation in Q2 2022, after an average review of 9.8 months. This takes the average duration of Phase I remedy investigations to 9.4 months over the first half of 2022, a nearly eight percent decrease compared to average duration of Phase I remedy cases in 2021, possibly indicating a return to pre-pandemic timelines.

Looking forward, the number of EU filings continues to trend high, although slightly below the 2021-record number. In contrast, the EC intervention rate is further decreasing, with fewer significant investigations conducted at the EU level.

The Intervention Rate is Dropping in Both the U.S. and the EU

In our last two reports, we have highlighted that the proportion of total notified transactions that receive significant investigations (the “intervention rate”) has fallen in recent years. Those trends have continued over the last quarter.

Estimating the exact intervention rate can be difficult because the length of concluded significant investigations varies. The best we can do is look at the significant investigations that have been concluded, when those transactions were filed, and the number of transactions that were notified over the same period.

In the United States, when we look at that data by quarter for HSR filings made going back to Q1 2019, we see a considerable drop in the intervention rate for HSR filings made since Q4 2020.

It is important to keep in mind that these figures only reflect significant investigations concluded as of June 30, 2022. Given the average duration of significant investigations, there are likely deals that were notified (for 2021 in particular) that are still subject to significant investigations that have not yet concluded.

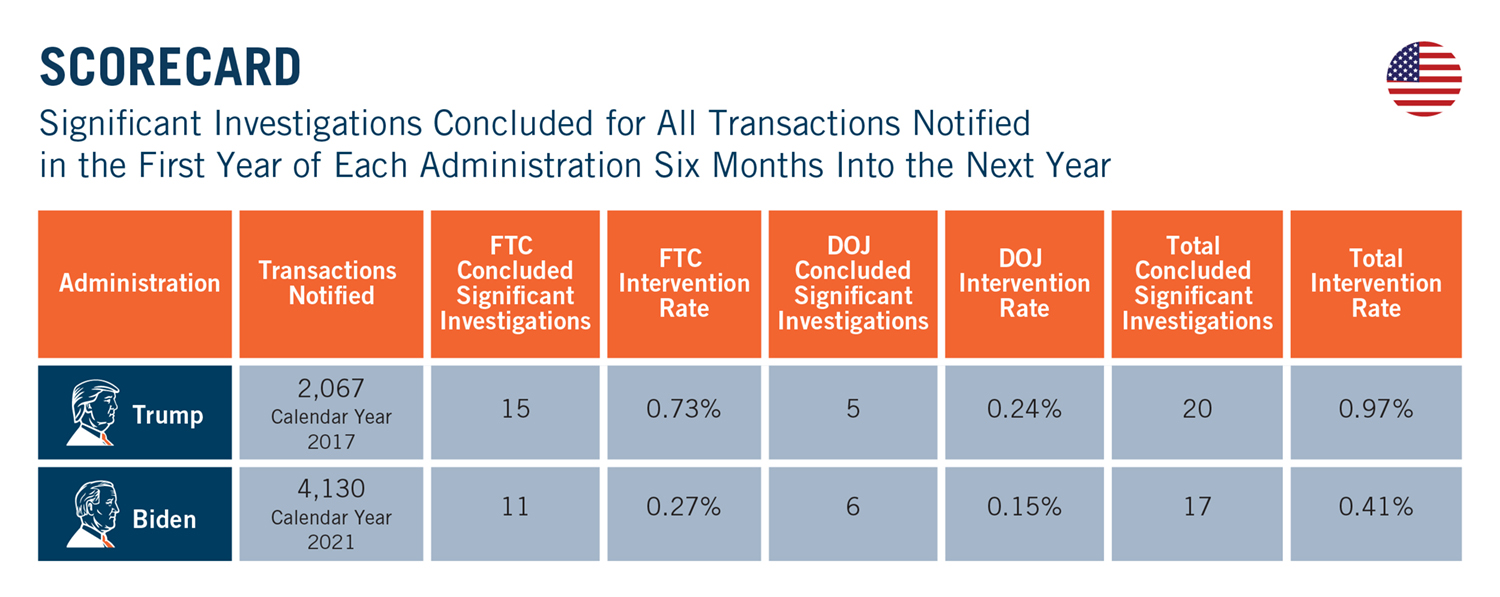

Nevertheless, our data show that the intervention rate for transactions notified in the first year of the Trump administration was more than double the intervention rate for transactions notified in the first year of the Biden administration at the same point in time. While the agencies received less than half of the number of notified transactions in the first year of the Trump administration, they had concluded three more significant investigations related to those transactions within six months after the year had ended.

Looking beyond Q2 2018, the U.S. antitrust agencies concluded 11 more significant investigations of deals that were filed in 2017, such that the final intervention rate for transactions notified in 2017 was 1.5 percent. To match that same final intervention rate for transactions filed in the first year of the Biden administration, the U.S. antitrust agencies would need to conclude 45 more significant investigations for deals filed in 2021. Based on the current data, it is highly unlikely that the intervention rate for the first year of the Biden administration will even come close.

The EU data shows a similar trend. Looking at the number of EU filings since Q1 2019, and the number of such filings that resulted in a significant investigation, there is a marked drop as of Q3 2020. While, on average, six percent of deals filed between Q1 2019 and Q2 2020 led to a significant investigation, only three percent of the filings submitted between Q3 2020 and Q4 2021 triggered a significant investigation.

Taking into account ongoing investigations on the EU side, data show that this downward trend continues in 2022, with an intervention rate averaging two percent for the first half of the year.

The recent ruling in the Illumina/Grail case could affect this trend in the EU. More than a year after the EC adopted a new approach to Article 22, only two cases have been referred under this provision, both resulting in a Phase II investigation. The limited use of this tool so far could have been linked to the uncertainty surrounding the new approach following Illumina’s appeal to the General Court of the EU against the referral of its deal. With the General Court greenlighting the EC’s approach on 13 July 2022, however, we may see an increased number of deals subject to article 22 referrals – unless national competition authorities decide to wait until the final ruling of the Court of the Justice of the EU on Illumina’s further appeal against the General Court judgement before starting to make real use of this mechanism.

Conclusion

Parties to transactions subject to significant merger investigations continue to face an elevated risk of seeing their deal blocked or abandoned, even if the intervention rate shows fewer deals as a percentage of merger filings may receive scrutiny. To ensure the ability to defend their deals through a potential investigation, parties to the average “significant” deal in the U.S. should plan on at least 12 months for the agencies to investigate their transaction and may want to add on additional time to address the continuing uncertainty at the agencies. Parties should also plan for another seven to nine months if they want to preserve their right to litigate an adverse agency decision. On the EU side, parties to transactions likely to proceed to Phase II investigations should allow for at least 19 months from announcement to clearance and should not rely on the theoretical deadlines provided for in the EU Merger Regulation, even after the deal has been formally notified. If the investigation is likely to be resolved in Phase I with remedies, parties should plan on around 10 months from announcement to a decision.

Related Professionals

Subscribe to Dechert Updates