DAMITT Q3 2021: Where’s the Wave? No Uptick Yet in Significant Merger Enforcement Activity

October 28, 2021

Key Facts

United States

- Dechert has yet to see an increase in concluded significant U.S. merger investigations despite a surge in merger filings that began in the fall of 2020. Instead, we continue to see a decrease in concluded significant merger investigations year-to-date compared to this point in 2019 and 2020.

- The average duration of significant merger investigations remains around 12 months, with significant variations below and above the average.

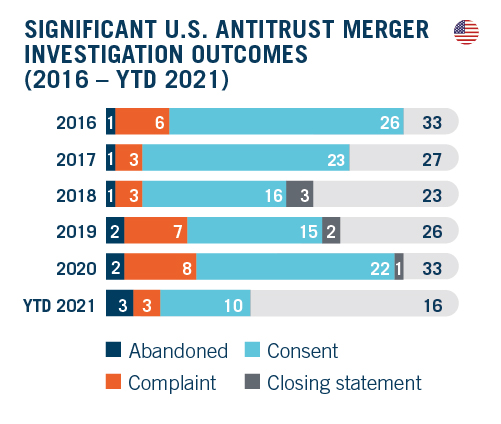

- The Federal Trade Commission did not file a single complaint or consent decree in the third quarter, which may suggest that it is taking longer for consent decrees to be finalized under the new administration.

European Union

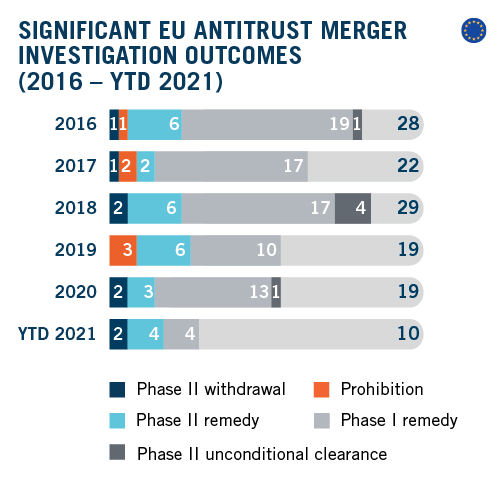

- The number of significant EU merger investigations concluded this quarter remained below average. Only two investigations were cleared with remedies, one in Phase I and one following a Phase II investigation. The number of deals notified so far in 2021 is, however, still significantly above 2019 levels during the same period.

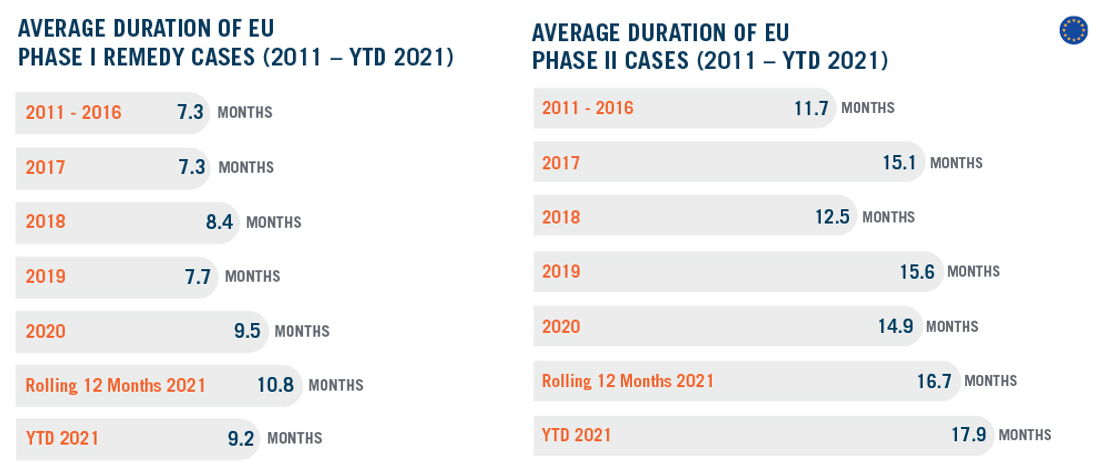

- The durations of both investigations were broadly in line with previously observed averages, bringing the 2021 average duration to 9.2 months for Phase I with remedies and 17.9 months for Phase II investigations.

- The seven currently pending Phase II investigations lasted on average more than 10 months from announcement to filing, the highest average duration observed since 2011, which may explain the low number of concluded investigations.

The Dechert Antitrust Merger Investigation Timing Tracker (DAMITT) is a quarterly study from Dechert LLP’s Antitrust/Competition practice reporting on trends in significant merger control investigations in the United States (U.S.) and European Union (EU).

In the U.S., “significant” merger investigations include Hart-Scott-Rodino (HSR) Act reportable transactions for which the result of the investigation by the Federal Trade Commission (FTC) or the Antitrust Division of the Department of Justice (DOJ) is a consent order, a complaint challenging the transaction, an official closing statement by the reviewing antitrust agency, or the abandonment of the transaction with the antitrust agency issuing a press release.

In light of the procedural differences between the EU and U.S., DAMITT defines “significant” EU merger investigations to include transactions subject to the EU Merger Regulation (EUMR) and resulting in either a Phase I remedy or the initiation of a Phase II investigation.

DAMITT calculates the durations of significant investigations in both jurisdictions from the deal announcement date through the completion of the investigation, and therefore includes the time attributable to pre-notification consultation efforts.

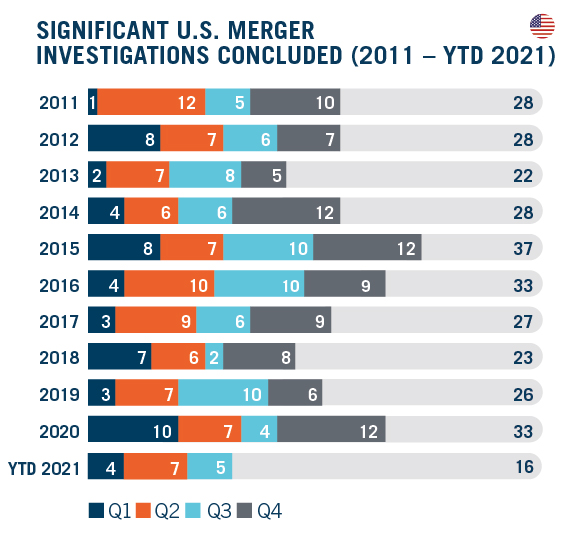

The Duration and Number of Significant U.S. Merger Investigations Show No Signs of a Surge

The 11.9-month average duration of significant U.S. merger investigations concluded so far in 2021 is comparable to the average duration in 2019 and 2020.

Similarly, the 16 significant U.S. merger investigations concluded during this period falls somewhat below the average at the same point each year over the last decade.

Given FTC warnings about a “surge” of HSR filings last Fall, which led the FTC and DOJ to suspend grants of early termination of the 30-day HSR waiting period in February, the data depict what might feel like the calm before a storm. Assuming that the increase in overall HSR filings will lead to at least some uptick in the number of significant U.S. merger investigations, we would expect to begin seeing an increase in the number of significant U.S. merger investigations concluded as we reach a year after the initial surge begun. We have not seen that surge yet. To the contrary, the FTC did not file a single complaint or consent decree in the third quarter.

While caution is typically warranted when inferring trends from an absence of data, the paucity of significant investigations concluded one year after the start of the reported surge in filings does suggest, if anything, that merger review periods are not getting shorter. This is consistent with recent statements from the Director of the Bureau of Competition that the FTC is making the second request process more rigorous.

Similarly, the FTC Commissioners may be asking for more time to scrutinize consent decrees, with Commissioners Chopra and Slaughter emphasizing in a Joint Concurring Statement in the Seven & i Holdings Co., Ltd. / Marathon Petroleum matter that “it was important to take the few extra weeks necessary to ensure that the resolution would effectively preserve competition and that any risk would be borne by the parties, not by consumers, workers, and other market participants.” Longer time frames for reviewing consent decrees in particular would help to explain the relatively low proportion of consent decrees so far this year compared with complaints and abandoned transactions.

Taken together, there is reason to believe that the average duration of recorded significant U.S. merger investigations concluded will increase in future quarters as we begin to see more of the results from investigations that began with the initial surge of HSR filings a year ago.

The Number of Concluded Significant EU Merger Investigations Remains Below Average Despite Surge in Merger Activity, Hinting Towards Longer Investigations

The EU Commission concluded only two significant merger investigations this quarter, bringing the total of significant investigations in 2021 to ten, 30 percent below the average at the same point of each year over the last decade.

This does not however indicate a decrease in merger activity; the number of deals notified so far in 2021 is back to normal and even above 2019 levels over the same period, and the number of decisions adopted by the EU Commission is on track to set a new record. But significant investigations represented only three percent of all decisions adopted thus far in 2021, compared to an average of six percent over the last decade.

While it is difficult to infer any general trend from a limited dataset, our view is that this does not signal a decrease in enforcement. The Commission appears to be issuing swift clearances in straightforward cases. 82 percent of the transactions approved in 2021 were cleared following a simplified procedure (which is only available for inherently unproblematic deals); this is higher than the previous annual averages of 80 percent in 2020, and 72 percent over the 2011-2020 period. However, the increasing duration of significant investigations appears to indicate that the Commission is struggling to conclude more complex deals without delays, possibly due to COVID-19-related difficulties it is facing.

While the small sample of decisions concluded this quarter – and so far this year – limits the value of any calculated average duration, the average duration of Phase II investigation is trending higher. The 2021 average duration to date has reached nearly 18 months, over a month longer than the previous 2015-record duration of 15.6 months. This trend towards longer Phase II investigations is unlikely to reverse in the short term; pending Phase II investigations have already clocked an average of nearly 18 months, including 10 months in pre-notification, the highest average observed since 2011.

Similarly, although duration of investigations of concluded in Phase I with remedies seemed to stabilize slightly above nine months, looking at average duration on a rolling 12-month basis suggests that the average duration may soon reach more than 10 months. The fact that the first Phase I significant investigation concluded in Q4 by the EU Commission lasted nearly 11 months appears to reinforce this hypothesis.

Conclusion

As of Q3 2021, the number of significant U.S. merger investigations concluded in 2021 is still behind historical averages for numbers of mergers concluded at this point of the year for most of the last decade. The average duration of those investigations was just under 12 months. Given the disconnect between the surge in HSR filings observed last Fall and the lower number of concluded investigations so far this year, there is reason to suspect durations for yet-to-be concluded matters are ticking upwards. These suspicions are bolstered by FTC statements about the increasing rigor of second requests and the increasing scrutiny required for consent decrees. As a result, parties to the average “significant” deal in the U.S. should plan on at least 12 months for the agencies to investigate their transaction and may want to add on additional time to address the continuing uncertainty at the agencies. Parties should also plan for another 7-9 months if they want to preserve their right to litigate an adverse agency decision.

Mirroring what is observed in the U.S., the number of significant EU merger investigations concluded so far in 2021 is also significantly below average. As the number of notified deals and adopted EU Commission decisions are above average, there is reason to believe that the decreasing proportion of significant EU merger investigations concluded so far may at least in part be due to the ever-increasing duration of significant EU merger investigations. Parties to transactions likely to proceed to Phase II investigations in the EU should allow for at least 18 months from announcement to clearance under the current circumstances. If the investigation is likely to be resolved in Phase I with remedies, parties should plan on around ten months from announcement to a decision.

Related Professionals