DAMITT Q1 2026: Restrained Merger Enforcement Continues But With Shorter Timelines

April 29, 2026

DAMITT, the Dechert Antitrust Merger Investigation Timing Tracker, is the leading source of analysis for significant U.S. and EU antitrust merger investigation and litigation trends.

Key Facts

United States

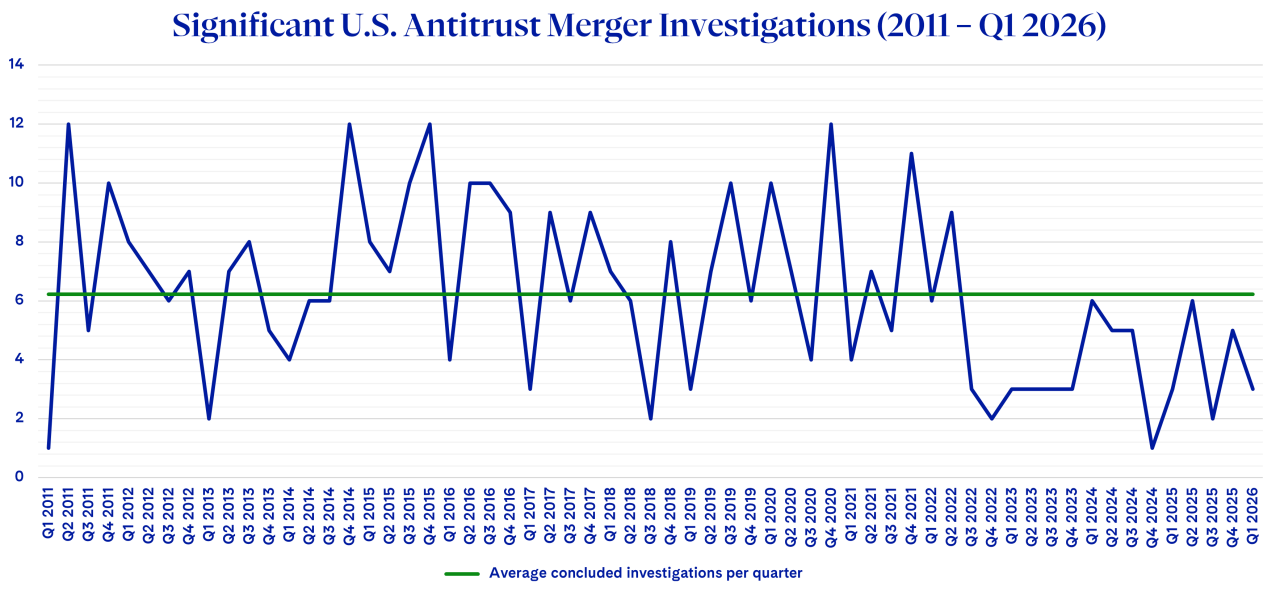

- With only four significant U.S. merger investigations concluded in Q1 2026, merger enforcement activity remains subdued, continuing a multi‑year trend tracing back to the Biden administration.

- The Trump administration’s revival of settlements with a reduction in litigations is contributing to a more deal-friendly antitrust environment compared to the Biden era.

- U.S. significant merger investigation timelines show recent improvement, with significant investigations of deals announced in 2025 finishing about a month faster on average than those concluded in 2024.

- Although the Trump administration reinstated early terminations in March 2025, the agencies are granting them far less frequently than before the 2021 suspension at rates well below historical norms.

European Union

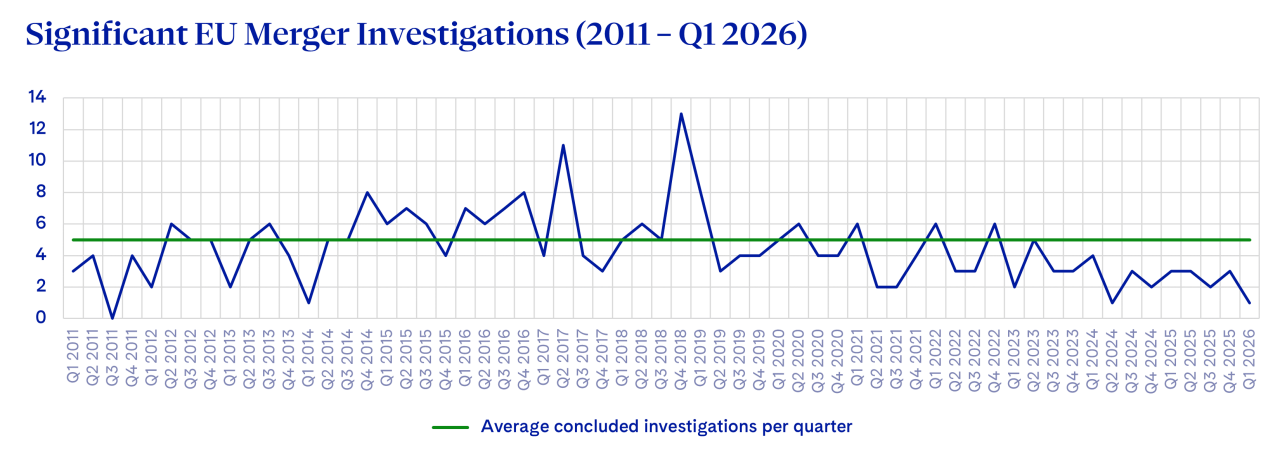

- The European Commission concluded only one significant merger investigation in Q1 2026 – a Phase II clearance with remedies – with no Phase I remedy decisions issued during the quarter, confirming the low enforcement trend observed over the past few years.

- The average duration of Phase II cases in Q1 2026 stood at 14.1 months, continuing the normalization trend from 2025’s 15.5 months and approaching the 2017–2020 average of approximately 14.5 months.

- A first draft of the revised Merger Guidelines is expected imminently, with a timeline for the adoption of the new guidelines currently in Q4 2027.

United States

Significant Merger Investigation Activity Continues Relatively Low Trend

The second year of President Trump’s second term has continued at a measured merger enforcement pace. In the first quarter of 2026, the Department of Justice (DOJ) and Federal Trade Commission (FTC) concluded four significant merger investigations – fewer than in the prior quarter but in line with the average quarterly volume observed last year. Overall activity remains near the historical first‑quarter norm of 4.8 investigations.

Although merger enforcement activity often fluctuates from quarter to quarter, DAMITT has observed a sustained decline in significant merger investigation outcomes per quarter since Q2 2022. By this measure, the low Q1 2026 count is consistent with this broader trend of reduced significant merger enforcement activity in the U.S. tracing back to the last two years of the Biden administration.

For most of DAMITT history, quarters with fewer concluded significant merger investigations often are followed by quarters with more activity. The agencies have averaged about 6.2 significant merger investigations per quarter over the past 15 years, but the sharp fluctuations of the pre‑Biden era have given way to a steadier and comparatively restrained enforcement cadence since Q2 2022. By comparison, during President Trump’s first term (2017–2020), the agencies averaged 6.8 significant merger investigations per quarter.

U.S. Agencies Continue to Favor Settlements Over Litigations

Even as significant U.S. merger investigations remained subdued, DOJ and the FTC secured three consent settlements in Q1 2026, underscoring a sustained revival of negotiated remedies in contrast to their limited use under the Biden administration, particularly in its final two years. This settlement pathway is creating a more deal-friendly antitrust environment as it reduces the risk that transactions will entirely collapse due to antitrust scrutiny.

The FTC recorded one merger abandonment (Alcon/Lensar) in the first quarter of 2026, marking only the second recorded abandonment during President Trump’s second term. At the current rate, the Trump administration’s second term is on pace to match or slightly exceed the six abandonments logged during President Trump’s first term.

Neither the DOJ nor the FTC filed any contested merger complaints in the first quarter of 2026. Currently, the agencies have only one active merger challenge pending (Henkel/Liquid Nails). Notably, a coalition of state attorneys general filed a complaint to block Nexstar’s acquisition of Tegna – even after the transaction was cleared by both the DOJ and the Federal Communications Commission – and successfully obtained a preliminary injunction preventing the companies from integrating operations pending a trial on the merits. Several states also intervened last year in the Tunney Act proceedings challenging the DOJ’s proposed consent decree in HPE/Juniper. In addition, three states – California, Colorado, and Washington – have enacted “mini-HSR” laws to get access to federal merger filings. Together, these actions signal the potential for more aggressive merger enforcement by states that disagree with their federal counterparts.

Early Signs That U.S. Merger Review Timelines May Be Shortening After Recent Historic Highs

The average duration of significant U.S. merger investigations concluded in Q1 2026 is 10.8 months, coming in below the 12.3-month record-high average in 2025. The year‑to‑date median investigation duration is 11.8 months, compared with a median of 11.6 in 2025.

For deals announced in 2025 and reviewed entirely under Trump-led agencies, the average investigation duration is 10.2 months, indicating some movement toward a shortening in average duration under the current administration. This shorter timeline may reflect an effort to recalibrate the pace of merger investigations, consistent with broader policy signals from agency leadership favoring a more streamlined approach to merger review – or, as FTC Chair Andrew Ferguson put it, a desire to “get out of the way” of unproblematic deals. Earlier this month, the FTC also reaffirmed in its mission statement that it will vigorously enforce the antitrust laws “without unduly burdening legitimate business activity,” a phrase that had been removed from the Biden FTC’s strategic plan.

Other recent developments may also contribute to shorter deal review timelines. A district court recently vacated the FTC’s new HSR rules implemented in February 2025, leading to the FTC’s reinstatement of the pre-February 2025 HSR form. The prior form imposed significantly less extensive filing requirements on merging parties, reducing the time needed to prepare HSR forms.

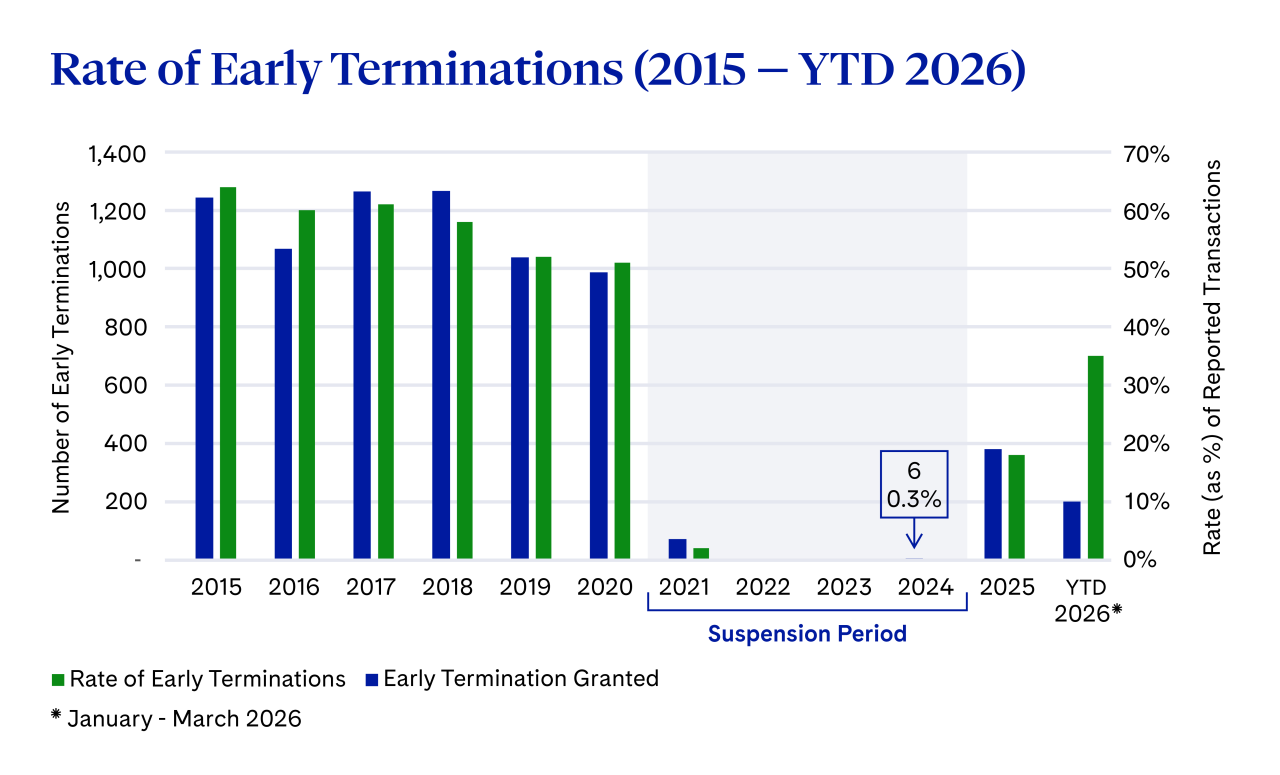

The current administration also resumed the practice of granting early termination notices in March 2025, following a suspension that had been in place since February 2021 under President Biden. As noted in the 2025 DAMITT Annual Report, DOJ leadership cited the return of early terminations as evidence of the agency’s efforts to “restore speed and efficiency to merger reviews.”

To assess how this policy shift has translated into practice, DAMITT compared the rate of early terminations since reinstatement with the rates observed prior to the February 2021 suspension.

As shown in the chart below, early terminations currently account for a substantially smaller share of reported transactions than in the pre‑suspension period. In 2025, the agencies granted early termination in just 18% of reported transactions (or 24% of transactions reported since the resumption, from March 2025 through March 2026), well below the 50–64% rates observed from 2015 through 2020. The current figure may have been partially impacted by the government shutdown during 2025, when the antitrust agencies were unable to grant early terminations for a short period. But even accounting for that distortion, early‑termination rates remain meaningfully below historical norms. In recent months, there are signs of modest improvement: the early‑termination rate has trended upward, reaching 35% of reported transactions for the first three months of 2026.

European Union

A Slow Start into the New Year: Q1 2026 Sets a Record Low in EU Merger Control Enforcement

Merger control enforcement activity reached a record low in the first quarter of 2026. Only one significant investigation outcome was recorded – a Phase II clearance with remedies. The downward trajectory in EU merger enforcement continues unabated.

Q1 2026 marks a decade-low since Q1 2014, matched only once before in Q2 2024, when the Commission had also completed only one significant investigation. Even taking into account Q1’s usual seasonal dip, this quarter stands out compared to the past three years where two significant investigations had been completed in 2023, four in 2024, and three in 2025.

Mirroring the conclusion on the US side, the variability that once characterized quarter-to-quarter enforcement has given way to a pattern of consistently low enforcement. Since Q2 2021, only two quarters exceeded the historical average of around 4.5 – Q4 2022 with six significant investigations concluded and Q2 2023 with five. With only two in-depth investigations opened in late 2025 and none in Q1 2026, the pipeline offers little reason to expect a sharp reversal in the near term.

Back to Normal? Phase II Duration Continues to Normalize

With only one Phase II decision in Q1 2026, in the Universal Music Group (“UMG”)/Downtown case, conclusions are difficult to draw. Yet, the duration of this case is consistent with the reduction in Phase II timelines observed in 2025.

After peaking at 19.35 months over the 2021–2024 period, the average Phase II duration fell to 15.5 months in 2025 – in line with the 2017–2020 average of approximately 14.5 months, though still above the 2011–2016 baseline of 11.7 months. At 14.1 months, the Q1 2026 case confirms the downward trend towards the 2017–2020 average.

Of interest in UMG/Downtown is the nature of the European Commission's concerns. These did not arise from the horizontal overlaps between the parties’ activities but were related to UMG’s possibility, after the transaction, to access competitors' commercially sensitive data through Curve, a Downtown subsidiary which runs a service platform processing information on artist-label relationships. The theory of harm in this case and nature of the commitments offered could explain why it went to Phase II instead of being swiftly resolved in Phase I.

Merger Guidelines Reform: A First Draft in Sight, But No Immediate Change

This historically low level of activity unfolds against the backdrop of the ongoing revision of the EU Merger Guidelines. The process is advancing steadily: following a public consultation that ran from May to September 2025 and two technical stakeholder workshops held in December 2025 and January 2026, Executive Vice-President and Commissioner Teresa Ribera has indicated that a first draft of the revised guidelines is expected on 30 April 2026. Full adoption remains targeted for Q4 2027. As such it remains to be seen if the revised framework will translate into a rebound in significant investigations.

Conclusion

United States

Parties to transactions subject to significant merger investigations continue to face an elevated risk of seeing their deals blocked or abandoned on both sides of the Atlantic. To ensure the ability to defend their deals through a potential investigation, parties to the average “significant” deal in the U.S. should plan on up to 11 months for the agencies to investigate their transaction. Parties should also consider allocating an additional 6-12 months in their transaction agreements if they want to preserve their right to litigate an adverse agency decision, for a total of 17-23 months.

European Union

On the EU side, Q1 2026 offers only little insight into enforcement trends. Parties to transactions likely to attract Commission scrutiny should identify early in the process remedies that could be offered to push for a swift outcome or, in case of a Phase II, plan for a minimum of 15 months from announcement to clearance.

Related Professionals

Subscribe to Dechert Updates